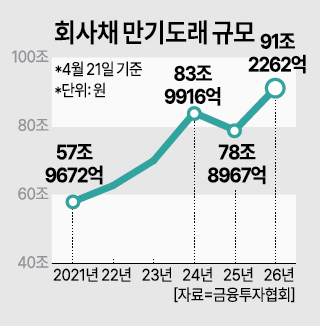

Corporate bond maturities due this year are expected to exceed 91 trillion won, a record that is pushing companies to prioritize refinancing over new investment. If the policy rate rises in the second half of the year, interest costs could jump further, raising concerns about weaker investment and hiring and broader financial-market stress.

The Korea Financial Investment Association said that as of Monday, corporate bonds maturing this year totaled 91.2262 trillion won. That is the highest level since the data series began, up 12.3295 trillion won from last year’s 78.8967 trillion won. Maturities in the first half amount to 57.8962 trillion won, or 63.4% of the total, concentrating repayment pressure early in the year.

Much of the debt was issued in 2020 and 2021, when ultra-low rates of about 1% to 2% enabled companies to raise large sums to secure liquidity. Since then, the market backdrop has shifted with policy-rate increases and Middle East-driven geopolitical risks, leaving firms to refinance those bonds at far higher rates.

With the Bank of Korea’s rate-cutting stance effectively over, upward pressure on rates has returned amid external factors including the possibility of a supplementary budget and a sharp rise in Japanese government bond yields. As of March 23, yields on three-year AA- rated corporate bonds rose to 4.197%, while BBB- rated bonds climbed to 9.979%.

Markets increasingly expect the central bank could raise the policy rate once or twice in the second half of the year. That would likely push refinancing rates higher and add to companies’ interest burdens.

As funding conditions tighten, companies are focusing on short-term liquidity rather than expansion. Rising demand for working capital suggests firms are emphasizing survival over growth.

Higher interest costs are likely to squeeze research and development and capital spending, undermining competitiveness over the medium to long term. If that is compounded by reduced hiring and smaller performance bonuses, household income and consumption could also weaken, raising the risk of a negative cycle.

The strain is expected to be heavier for mid-sized and small businesses. Large companies may refinance more steadily thanks to cash holdings and stronger credit, but lower-rated firms, including those rated BBB or below, and many mid-sized and small companies could face a credit crunch that makes funding difficult. If refinancing fails or borrowing costs surge, some companies could face liquidity crises.

Policy factors are adding to the pressure. As the government encourages greater shareholder returns, companies face interest-payment burdens alongside demands for dividends and share buybacks, highlighting a dilemma between financial soundness and shareholder payouts.

Analysts say the path of interest rates could turn corporate debt into a broader drag on the economy. If rate hikes materialize in the second half, higher interest costs could deliver a combined shock that restrains investment, employment and consumption.

Jung Hwa-young, a research fellow at the Korea Capital Market Institute, said, “For lower-credit companies, interest expenses can rise quickly when profitability and financial soundness deteriorate.” She added, “Authorities need to closely monitor funding conditions for vulnerable firms and respond in a timely way to market instability.”

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.