South Korea’s two biggest chipmakers, Samsung Electronics and SK hynix, posted earnings surprises in the first quarter despite the usual seasonal slowdown. With results expected to accelerate into the second half, investor expectations are rising that their combined operating profit could reach 500 trillion won this year.

According to brokerage estimates cited on April 24, SK hynix is forecast to post 65.1 trillion won in operating profit in the second quarter, nearly double its first-quarter operating profit of 37.6 trillion won. Samsung’s second-quarter operating profit is projected at 89.9 trillion won. Together, that would total about 155 trillion won for the quarter.

The outlook reflects expectations that prices for DRAM and NAND flash — key drivers of the first-quarter improvement — will climb even more in the second quarter. Kim Hyeong-tae, an analyst at Shinhan Investment Corp., said average selling prices are expected to rise 41% for DRAM and 67% for NAND from the previous quarter, adding that the NAND market “is somewhat undervalued” and that expectations for a “surprise” NAND performance remain in place.

Even in the seasonal off-peak period, the two companies’ combined operating profit from their semiconductor businesses reached 90 trillion won in the first quarter. Of Samsung’s preliminary operating profit of 57.2 trillion won, operating profit from its semiconductor (DS) division is estimated at around 50 trillion won.

Profitability also hit record levels. SK hynix said in its earnings release on April 23 that it posted a 72% operating margin, well above the 58% reported by Taiwan’s TSMC, the top foundry company often seen as a benchmark for chip profitability. Samsung’s first-quarter operating margin was 43%, and its memory business alone is estimated to be in the 60% range.

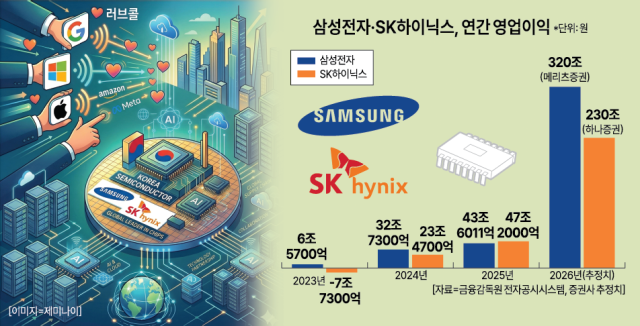

Brokerages are increasingly projecting that combined operating profit this year will exceed 500 trillion won. They forecast annual operating profit of 320 trillion won for Samsung (Meritz Securities) and 230 trillion won for SK hynix (Hana Securities), for a combined 550 trillion won.

Analysts also say memory chips are becoming core infrastructure in the AI transition, pointing to structural growth rather than a temporary boom. Choi Bo-young, an analyst at Kyobo Securities, said demand for DRAM and NAND is expanding broadly as agentic AI spreads, while a structural supply shortage persists, setting up steep price increases in the second half. Choi said SK hynix is seeing clearer gains in high-value products based on its HBM3E exclusivity and a 60% share in HBM4, and that long-term supply agreements (LTAs) have helped reduce earnings volatility and improve visibility for a longer cycle.

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.