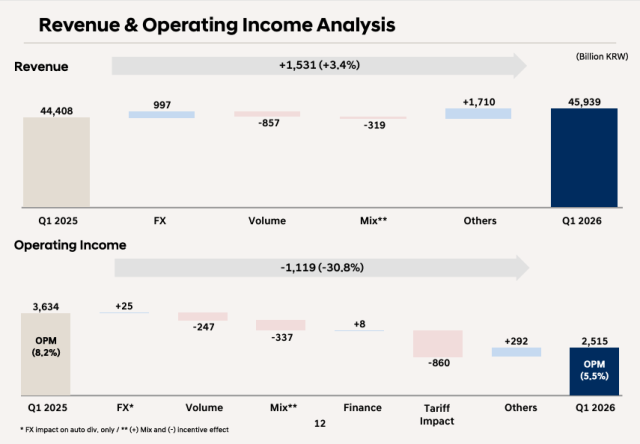

Revenue rose 3.4 percent year on year to 45.9 trillion won, marking the highest first-quarter figure on record. The increase was supported by strong sales of high-margin SUVs and hybrid vehicles, even as global industry demand contracted 7.2 percent.

Operating profit, however, fell 30.8 percent to 2.51 trillion won, with the operating margin narrowing to 5.5 percent from 8.2 percent a year earlier.

The result came in at the lower end of market expectations, with estimates compiled by FnGuide pointing to operating profit in the range of 2.4 trillion to 2.6 trillion won.

A breakdown of earnings drivers showed that tariff-related costs were the single largest drag on profitability, reducing operating profit by 860 billion won. Lower volumes cut earnings by 247 billion won, while a weaker product mix — driven by higher incentive spending — reduced profit by a further 337 billion won.

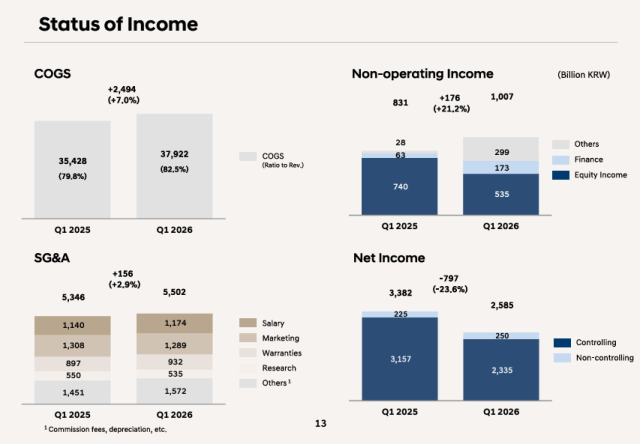

Cost pressures were also evident in the company's structure, with the cost of sales rising to 82.5 percent of revenue, up 2.7 percentage points from a year earlier, driven largely by higher raw material prices.

It also acknowledged production disruptions following a fire at a key engine valve supplier, though it expects to normalize output from April and recover lost production in the second half through global production adjustments.

Regional dynamics also weighed on profitability. Incentive spending remained elevated in Europe amid tightening emissions regulations, while India emerged as a rare bright spot, with record sales and minimal incentive burden.

Despite pressure in its core automotive business, Hyundai's financial arm delivered stable earnings growth supported by asset expansion, partially offsetting the decline in vehicle operations.

Looking ahead, the company said it is accelerating autonomous driving development through collaboration with Nvidia to secure data and enhance competitiveness. It is also shifting its China strategy toward export-driven growth, with exports already accounting for around 40 percent of local sales.

Shares of Hyundai Motor closed at 532,000 won, down 1.7 percent on the day.

Copyright ⓒ Aju Press All rights reserved.