The prolonged conflict between the United States, Israel and Iran has sharply disrupted energy supply chains across Asia, with tanker traffic through the Strait of Hormuz grinding to a halt after Iran shut down the strategic waterway following joint U.S.–Israeli strikes on Feb. 28.

For South Korea — one of the world's largest importers of energy and petrochemical feedstock — the shock is hitting an industry already weakened by Chinese overcapacity and falling margins.

About 54 percent of the country's naphtha imports and roughly 70 percent of its crude oil typically pass through the strait, leaving domestic refiners and petrochemical producers acutely exposed to a prolonged blockade.

Naphtha prices have surged about 55 percent since the conflict escalated, jumping to $883.4 per metric ton on March 9 from $568.55 on Feb. 23, according to the Naphtha FOB Fujairah Cargo Assessment compiled by S&P Global Platts.

Oil markets have also experienced extreme volatility. U.S. benchmark West Texas Intermediate traded around $89.96 per barrel after swinging within a roughly $28 range, while global benchmark Brent crude stood at $88.87, sharply below an intraday peak of $119.50 reached earlier in the conflict.

The disruption has pushed the East-West naphtha spread above $50 per ton for April contracts, more than $30 higher since the start of the year, reflecting mounting concerns over reduced Middle Eastern supply into Asia, which normally receives roughly 40 percent of global naphtha exports from the Gulf region.

Forward structures have tightened sharply as well, with April–May timespreads widening by about $20 per ton in both Asian and European benchmarks, approaching levels last seen at the start of the Russia-Ukraine war in 2022.

The market is increasingly pricing in shortages as buyers scramble to secure replacement cargoes from Europe and the United States.

The supply shock is already forcing petrochemical producers to cut operating rates.

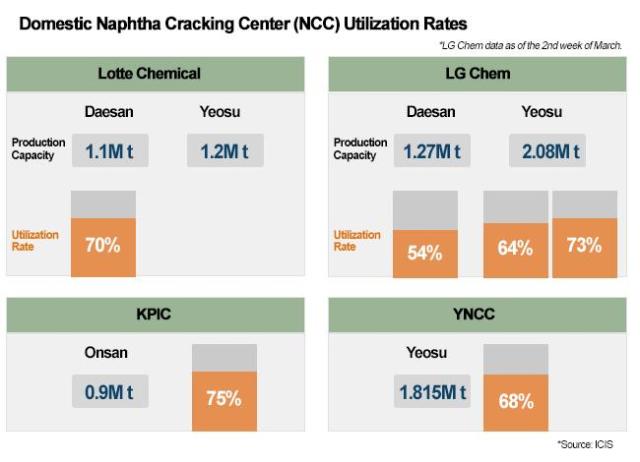

LG Chem is lowering operating rates at its Daesan facility from 69 percent to about 54 percent and trimming output at its Yeosu complex.

Korea Petrochemical is reviewing a reduction from 80 percent to roughly 75 percent at its Onsan plant.

Yeochun NCC — a joint venture between Hanwha Solutions and DL Chemical and one of South Korea's largest ethylene producers — declared force majeure on March 4, warning customers that naphtha deliveries for March would be significantly delayed.

Industry executives warn that the next month could prove decisive.

Petrochemical companies typically maintain around one month of naphtha reserves, meaning prolonged disruptions could force deeper production cuts or temporary plant shutdowns.

The squeeze is intensified by a structural pricing trap: surging feedstock costs cannot easily be passed on to buyers because persistent Chinese oversupply continues to depress prices for ethylene and downstream petrochemical products.

Analysts say the pattern echoes the early phase of the Russia-Ukraine war, but the impact could prove more severe given Asia's heavier reliance on Middle Eastern feedstock.

"If the war is not resolved within the next week, further price spikes are inevitable as inventories deplete and panic buying intensifies," said Yoon Jae-sung, an analyst at Hana Securities.

"Should the disruption extend beyond two weeks, we could see a wave of plant shutdowns globally. Companies with lower dependence on Middle Eastern feedstock will be in a stronger position."

LNG shock adds further energy pressure

Energy costs are rising across the broader industrial system.

Qatar, which accounts for about 20 percent of global LNG supply, halted production at its Ras Laffan facility after Iranian drone and missile strikes on March 2 and declared force majeure on exports two days later.

South Korea imports roughly 20 percent of its LNG from the Middle East, largely under long-term contracts, but replacement volumes on the spot market are now significantly more expensive.

"It is the global supply-demand balance that determines LNG prices," said Roh Nam-jin, senior researcher at the Korea Energy Economics Institute.

"Even though South Korea relies relatively less on Middle Eastern LNG compared with oil, a broad increase in LNG prices will inevitably affect the domestic energy market."

About half of South Korea's imported LNG is used for electricity generation, which accounts for roughly 30 percent of national power output, meaning higher LNG costs could eventually push up industrial electricity prices.

Restructuring gains momentum but faces new obstacles

The crisis comes as the petrochemical sector is already undergoing a painful restructuring.

Hanwha Solutions and DL Chemical recently agreed to shut down two of Yeochun NCC's three plants, reducing ethylene capacity from 2.3 million tons annually to about 900,000 tons.

The remaining operations will later merge with Lotte Chemical's Yeosu complex, which has annual capacity of 1.23 million tons, to form a new joint venture expected this year.

The restructuring follows the government-backed "Daesan No.1 Project," which merged operations between Lotte Chemical and HD Hyundai Chemical with a 2.1 trillion won ($1.42 billion) support package.

Yeochun NCC's financial position had deteriorated rapidly even before the war. Its operating losses widened from 150.3 billion won in 2024 to 198.9 billion won in the first nine months of 2025, leaving the company close to default last year.

The government approved financial support for the Daesan restructuring on Feb. 25 and is expected to extend similar backing for the Yeosu plan.

Labor law adds uncertainty to industry overhaul

But the restructuring process now faces a new complication.

South Korea's revised labor union law — widely known as the Yellow Envelope Law — takes effect Tuesday, expanding the scope of legally permissible labor disputes to include corporate restructuring and business reorganization.

The law also allows subcontractor unions to demand collective bargaining directly with parent companies, a provision that could complicate plant closures or workforce reductions at petrochemical complexes that rely heavily on subcontracted labor.

Industry officials warn that the convergence of war-driven feedstock shocks, structural overcapacity and regulatory uncertainty leaves the sector with limited room to maneuver.

If the Hormuz blockade persists and feedstock inventories run out, utilization rates at domestic naphtha cracking centers could fall below 60 percent, with ripple effects spreading across downstream industries including electronics, automotive manufacturing, construction materials and consumer goods.

Copyright ⓒ Aju Press All rights reserved.