A recent analysis indicates that securing liquidity is essential for the early establishment of the domestic asset tokenization market in South Korea.

According to the "BOK Issue Note: Current Status and Future Policy Tasks of Domestic and International Asset Tokenization" published by the Bank of Korea on May 14, the cumulative size of fractional investments in South Korea reached approximately 640 billion won as of January. The global asset tokenization market was valued at $50.37 billion (about 75 trillion won) as of the end of March. The annual growth rate of the global tokenization market is projected to be 65% in 2023, 93% in 2024, and 169% in 2025, indicating rapid expansion.

Tokenization enhances the efficiency, flexibility, accessibility, and transparency of asset issuance, distribution, and payment methods. It integrates the entire transaction process through distributed ledgers, shortening settlement cycles and reducing intermediary and management costs. The domestic market is in the early stages of integrating distributed ledger technology with fractional investments in non-traditional assets such as real estate and music copyrights through regulatory sandboxes. In February 2026, a regulatory framework was established for the issuance and distribution of token securities.

Regionally, the United States accounted for 65.2% of the market as of the end of March, making it the largest player. Europe followed with 14.5%, and regulatory havens accounted for 14.4%. In Asia, Hong Kong (2.3%) and Singapore (0.8%) are working to promote the asset tokenization market through regulatory improvements and infrastructure development.

Despite the global tokenization market's growth, its size remains modest compared to traditional financial markets, and asset tokenization is not yet fully underway in South Korea, resulting in a low impact on financial stability at this time. However, the accumulation of vulnerabilities in the existing financial system or the emergence of new systemic risks could occur.

The Bank of Korea noted, "Tokenization can accumulate systemic vulnerabilities through increased leverage and interconnectivity," adding that "rapidly expanding leverage through re-collateralization could lead to a chain reaction of deleveraging during price declines."

Furthermore, it stated, "Operational, technical, and legal vulnerabilities could lead to a decline in market trust and transaction disruptions, potentially amplifying risks across the financial system." It also warned that if tokenized assets are issued and distributed across different blockchain networks rather than a single standard or common infrastructure, there is a risk of market fragmentation.

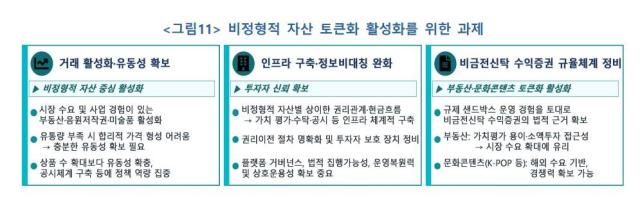

To ensure the early establishment of the domestic tokenization market, the Bank of Korea recommended securing liquidity, particularly for non-traditional assets such as real estate, music copyrights, and artworks, where market demand has been confirmed and business experience has been accumulated. It emphasized that without sufficient liquidity in the early stages of the tokenization market, rational price formation would be difficult, leading to weakened investor confidence due to inadequate trading.

Thus, it is crucial to focus policy efforts on creating a market where actual transactions occur through the formation of abundant liquidity and standardized disclosure systems, rather than merely increasing the number of products. Additionally, the Bank of Korea stressed the need to systematically establish core infrastructure for valuation, custody, disclosure, and investor protection to secure investor trust. It also highlighted the necessity of creating conditions for issuing token securities based on trust income certificates for real estate or music copyrights by establishing a legal basis for non-monetary trust income securities based on tangible and intangible assets.

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.