Equity markets in both countries are on fire. The KOSPI is up more than 85 percent this year, the Nikkei 225 more than 22 percent. Both economies have outperformed expectations, with Japan's GDP expanding 2.1 percent on an annualized basis in the first quarter and Korea's 1.7 percent, as tech-heavy manufacturers ride the AI boom.

But the robust headline numbers mask a colder reality the AI froth is hiding — dangerously high leverage, asset inflation, depopulation, energy shocks tied to heavy dependence on Gulf fuel sources, and stubbornly weak currencies.

Overlooked by euphoric equity investors, debt yields are rising sharply across major economies as inflation fears, oil shocks and mounting public debt collide with overheated asset prices.

Nowhere is that tension clearer than in South Korea and Japan — two export powers riding the AI wave while simultaneously confronting the return of inflation, currency weakness and bond-market stress.

Korea's producer price index surged 2.5 percent month-on-month and 6.9 percent year-on-year in April, the sharpest pace since the aftermath of the 1998 Asian financial crisis. Petroleum and coal prices jumped 31.9 percent, while financial and insurance services rose 26.2 percent — the largest increase on record — as stock trading exploded during the AI frenzy.

Brokerage commissions alone surged 119 percent as retail investors rushed into the market on fear of missing out. The KOSPI soared more than 85 percent between the end of 2025 and May 21, while consumer sentiment returned to optimistic territory despite accelerating inflation pressures.

Japan is experiencing a parallel dynamic.

The Nikkei 225 has climbed more than 22 percent this year alone, powered by AI-linked manufacturing, semiconductors and global capital flows seeking alternatives to slowing Western growth. At the same time, Japanese government bond yields have surged to levels unseen in decades as investors price in a more sustained exit from ultra-loose monetary policy.

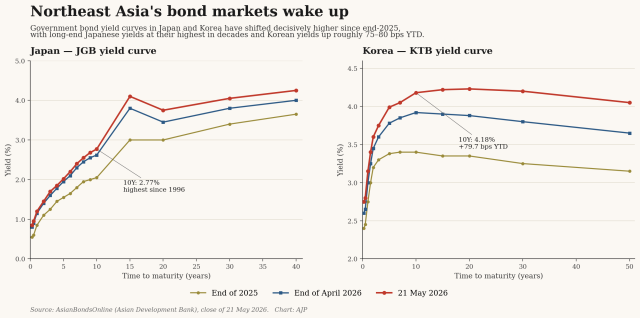

Japan's 10-year government bond yield climbed above 2.8 percent this week — its highest since 1996 — after stronger-than-expected economic growth reinforced expectations that the Bank of Japan may continue tightening. Thirty-year Japanese yields touched record highs dating back to 1999.

Korea's 10-year yield simultaneously climbed above 4.1 percent, while five-year yields approached 4 percent.

What links the two countries is not merely the AI rally itself, but the structural vulnerability hidden beneath it.

Both Korea and Japan remain deeply dependent on imported energy, external demand and globally mobile capital.

Both have allowed years of ultra-cheap liquidity to inflate financial assets. And both are now discovering that AI-driven wealth can quickly spill into inflation psychology, speculative behavior and currency instability.

The shift is already feeding through markets.

Foreign investors dumped a net 44.6 trillion won worth of KOSPI shares in May through May 21, after modest buying in April, according to Financial Supervisory Service data. Daily foreign selling reached nearly 2.94 trillion won on May 20 alone.

The exodus has intensified pressure on the Korean won. The dollar-won exchange rate climbed from 1,483.3 won at the end of April to above 1,506 this week, before surging further intraday Friday toward 1,518 amid broad foreign selling and dollar strength. One-month forward rates also jumped, signaling expectations for further depreciation.

That matters because neither Korea nor Japan imports inflation gently.

Both economies rely heavily on imported oil, gas and raw materials. Brent crude remains more than 72 percent above end-2025 levels, while Dubai crude is still up more than 56 percent despite recent pullbacks. A weaker won and weaker yen therefore magnify energy costs directly into domestic producer prices, transportation costs and household inflation.

And the AI boom itself is beginning to amplify those pressures.

In Korea, semiconductor profits and stock gains are reshaping wage expectations across industries. Samsung Electronics and SK hynix bonuses are becoming reference points far beyond the chip sector, fueling broader compensation demands during an already inflationary period. Retail participation in equities has surged as households increasingly treat asset inflation as a substitute for income growth.

Japan faces a different historical context but an increasingly similar outcome. After decades of wage stagnation, rising corporate profits and labor shortages are finally pushing salaries higher. But stronger wages combined with rising import costs are also complicating the Bank of Japan's long-awaited normalization process.

The central banks now face a dilemma with no painless solution.

If they keep policy loose, currencies may weaken further, feeding imported inflation and asset bubbles. If they tighten aggressively, they risk puncturing equity rallies and destabilizing heavily indebted governments and households accustomed to abundant liquidity.

This is why the recent bond-market moves matter far beyond technical finance.

Global investors are beginning to question whether the AI era can coexist indefinitely with the monetary assumptions of the post-2008 world — ultra-low rates, permanently suppressed bond yields and endless liquidity support.

That skepticism is appearing simultaneously across markets.

U.S. Treasury yields have climbed sharply amid inflation and debt concerns. German bund yields are approaching levels last seen during the eurozone sovereign debt crisis. British gilt yields are hovering near financial-crisis highs. Japan's long-dormant bond market is finally awakening. Korea's curve is steepening rapidly.

Bond vigilantes — long absent during the era of quantitative easing — are returning globally.

For Korea and Japan, the danger is particularly acute because both economies sit at the intersection of technology euphoria and external vulnerability. Their markets have grown increasingly dependent on foreign inflows, semiconductor optimism and weak currencies that support exports. But those same weak currencies now threaten to import inflation at precisely the moment asset markets appear most overheated.

History shows these phases can persist longer than expected. Asset rallies often intensify even as financial conditions deteriorate underneath. The Asian financial crisis began not with recession, but with confidence and capital inflows. So did many liquidity booms before it.

That does not mean a crisis is imminent. But it does mean the era of consequence-free liquidity is ending.

The AI revolution may indeed reshape the global economy. But it will not abolish the basic laws of finance. Rising wages, weaker currencies, higher oil prices and surging asset values eventually collide with the bond market's demand for discipline.

And that collision is beginning to unfold across Northeast Asia now.

Copyright ⓒ Aju Press All rights reserved.