SEOUL, March 12 (AJP) — South Korea’s largest companies have rushed to retire 36.3 trillion won ($25 billion) worth of treasury shares in the first quarter of 2026 under a new Commercial Act amendment, but analysts warn the mandatory move may do little to improve corporate value while stripping management of a key strategic tool.

A string of blue-chip firms including Samsung Electronics, SK hynix and Samsung C&T have unveiled large-scale treasury share cancellations since the revised law took effect, putting share buybacks and retirements at the center of Korea’s market reform drive.

Supporters say broader cancellations could help narrow the longstanding “Korea discount” by lifting per-share metrics and strengthening shareholder returns. Critics, however, say the law forces companies to give up assets long used to support management control, fund acquisitions and compensate employees.

The third amendment to the Commercial Act, passed by the National Assembly on Feb. 25 and effective from March 6, requires listed companies in principle to cancel treasury shares within a year of acquiring them. Exceptions, including stock-based compensation and employee stock ownership plans, are allowed only with shareholder approval at a general meeting.

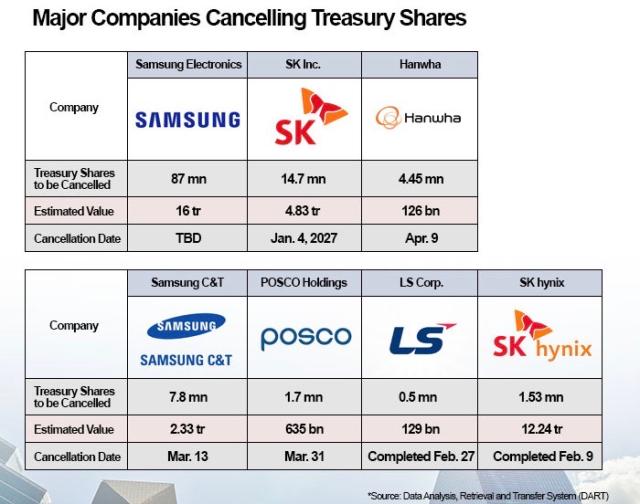

According to regulatory filings, Samsung Electronics plans to cancel about 87 million treasury shares worth roughly 16 trillion won. SK hynix will retire 15.3 million shares valued at about 12.24 trillion won.

Other major firms are following suit. Samsung C&T plans to cancel 7.81 million shares worth about 2.33 trillion won, while SK Inc. will retire 14.69 million shares worth around 4.83 trillion won. POSCO Holdings and LS Corp. have also canceled treasury shares worth about 635.1 billion won and 129.3 billion won, respectively.

Canceling treasury shares reduces the number of shares outstanding, which typically boosts earnings per share and book value per share. For that reason, it has long been regarded as a straightforward way to return value to shareholders.

But analysts say the effect on corporate value is not automatic.

“The idea that fewer shares automatically raise corporate value is too simplistic. Markets have already priced in such factors,” said Shin Hyun-han, a professor at Yonsei University.

Kim Dae-jong, a professor at Sejong University, said treasury share retirements can be a more equitable form of shareholder return than dividends because they benefit all shareholders proportionately. Even so, he cautioned that making cancellations mandatory could come at a high cost for companies.

“The biggest loss from mandatory cancellations is reduced capital flexibility,” Kim said. “Companies can sell treasury shares to raise cash or use them in M&A deals. Mandatory cancellations remove that option.”

Treasury shares have long served as strategic assets for Korean companies, despite being treated as a deduction from equity in accounting terms. In practice, they have functioned as a reserve of capital that can be mobilized for financing, strategic partnerships or management defense.

That matters especially in Korea, where treasury shares have at times played a role in reinforcing control structures during corporate restructuring or spin-offs. With forced retirements becoming the norm, those options could narrow, making it harder for controlling shareholders to defend management rights.

Shin argued that the broader risk is a decline in management stability.

“If management control can be easily challenged, companies may struggle to make long-term plans,” he said.

He also warned the rule could backfire by discouraging future buybacks altogether.

“If buybacks must ultimately be canceled, companies may avoid them and choose dividends instead,” Shin said, calling the policy “penny wise, pound foolish.”

For policymakers, the measure is meant to push listed firms toward stronger shareholder returns and more transparent governance. But for corporate Korea, the new mandate is fast turning treasury shares from a flexible strategic resource into a disappearing one.

Copyright ⓒ Aju Press All rights reserved.