SEOUL, April 13 (AJP) - South Korean sovereigns joining the World Government Bond Index (WGBI) hardly proved to be a magic wand for both the currency and bonds in the first month.

Extraordinary factors — including escalating Middle East conflicts and a shifting interest rate and inflation environment — have partly undermined the honeymoon period. Some experts say Korea’s structural challenges run too deep to rely simply on a WGBI boost.

Since FTSE Russell began including Korean bonds in the WGBI on April 1, authorities have highlighted expectations of strong foreign inflows to ease pressure on the won and bond market. Finance Minister Gu Yun-cheol reiterated that stance Friday, pointing to foreign net purchases of 6.8 trillion won ($4.57 billion) in government bonds so far this month.

Yet the impact on markets has been limited. Despite steady foreign buying, the won and bonds have shown little sign of relief. Entering its third week of inclusion, the Korean won closed Monday at 1,489.3 per dollar and has hovered near the 1,500 level — territory last seen in the aftermath of the 2008 global financial crisis.

The bond market has shown similar strain. The three-year government bond yield rose 4.7 basis points to 3.407 percent, while the 10-year yield climbed 5.7 basis points to 3.743 percent — still 30 to 40 basis points higher than at the start of the year.

Foreign participation has also underwhelmed relative to expectations. According to the Korea Financial Investment Association (KOFIA), foreign holdings of domestic bonds stood at 340.4 trillion won at the end of March, down 10.2 trillion won from a month earlier.

A key driver has been the shift in the rate environment. The Hyundai Research Institute warned that if Middle East maritime disruptions persist and oil prices exceed $100 per barrel, South Korea’s consumer inflation could rise to 3.1 percent — more than one percentage point above the Bank of Korea’s 2 percent target.

That outlook is pushing the central bank toward a more hawkish stance. After removing references to a rate cut in January, the Bank of Korea is now widely expected to consider rate hikes as early as July, reinforced by the policy stance of governor-nominee Shin Hyun-song.

Major financial institutions, including Shinyoung Securities and Citi, say this shift is reducing the relative attractiveness of Korean bonds and diluting the impact of WGBI inclusion.

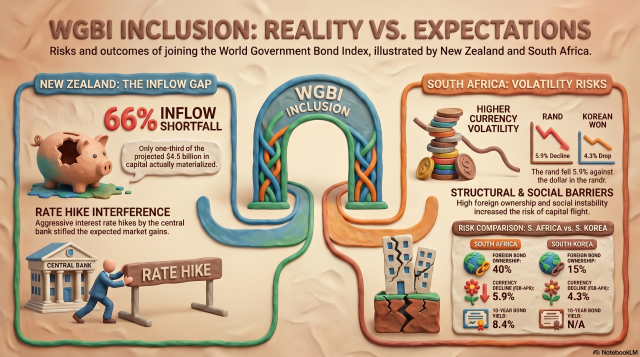

Such over-optimism is not new. New Zealand, which began phased inclusion in the WGBI in November 2022, initially expected $4.5 billion in inflows. However, aggressive rate hikes by the Reserve Bank of New Zealand in response to inflation reduced actual inflows to roughly one-third of that estimate.

South Africa offers a similar case. Despite high yields — with its 10-year bond yield around 8.4 percent — the rand weakened 5.9 percent as of April 7 from February levels, a steeper decline than the won’s 4.3 percent drop over the same period. Analysts attribute this to the high share of foreign ownership in South African bonds, about 40 percent compared with Korea’s 15 percent, which amplifies capital outflow risks. Broader structural factors, including social instability, have also weighed on investor sentiment.

Experts stress that strengthening economic fundamentals must take priority over one-off catalysts such as index inclusion. Reflecting concerns over Korea’s heavy reliance on Middle East energy supply chains, Natixis recently cut its growth forecast for the country to 1.0 percent from 1.8 percent, well below the OECD average of 1.7 percent.

“We must abandon the illusion that WGBI inclusion alone will dictate the trajectory of bonds and the exchange rate,” said Kim Chan-hee, an analyst at Shinhan Securities, pointing to the need to address structural vulnerabilities such as energy dependence.

Goldman Sachs echoed that view, noting that capital flows are driven primarily by global rates and risk sentiment rather than index events, and that improving the structural appeal of the Korean market remains key to supporting both the won and government bonds.

Copyright ⓒ Aju Press All rights reserved.