The real estate market is difficult to read. Owning a home is equally challenging. Government policies are no exception. This is where the tough 'real estate' perspective begins.

The administration of President Lee Jae-myung has focused on stabilizing housing prices, starting in Gangnam.

Since taking office, President Lee has prioritized housing price stabilization, stating, "We will do whatever it takes to control housing prices." He implemented a series of measures, including land transaction permits, total loan management, and the resumption of increased capital gains taxes for multiple homeowners. Gangnam was the target, as it symbolizes Seoul's housing market and serves as a litmus test for regulatory effectiveness.

On February 3, he shared a report on social media about an increase in listings in the three Gangnam districts, calling out reports claiming there was no effect or that listings were not emerging as "nonsense." However, after the third week of February, apartment prices in the three Gangnam districts began to decline, with Gangnam experiencing 12 weeks of stagnation or decline. Analysts noted that the cumulative regulations were holding back the Gangnam area, leading to comments that "this government is different," suggesting that the policies were having an impact.

However, the market responded differently.

On May 9, the exemption for increased capital gains tax for multiple homeowners ended. In the second week of May, apartment prices in Gangnam rose by 0.19%. The belief that the policies were effective began to waver, along with the expectation that taxes would drive listings out and suppress Gangnam prices.

Of course, one week of price increase cannot definitively determine the success or failure of a policy. What matters is not just the rate of increase but why Gangnam began to move right after the end of the capital gains tax exemption. This timing itself illustrates the paradox of the policy.

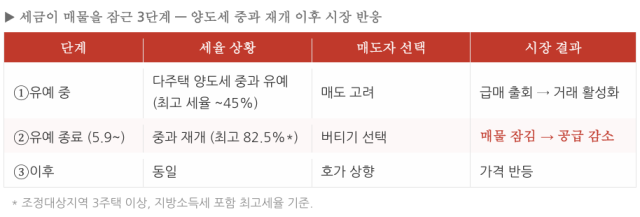

The moment taxes lock away listings

Taxes present sellers with two choices: sell now and pay taxes or hold off and wait. If the tax rate is manageable, taxes encourage sales, prompting sellers to list properties before the burden of ownership increases. This was the effect the policy aimed to achieve before the end of the capital gains tax exemption.

However, when the highest tax rate reaches 82.5%, including local income taxes, the calculations change. When sellers feel they will gain nothing from a sale, taxes become a deterrent rather than a motivator. The heavier the tax burden, the more listings tend to lock up rather than increase, creating a paradox.

Properties that were listed before the exemption ended were quickly absorbed. However, homeowners who remained after the exemption ended chose to hold onto their properties. According to the real estate big data platform Asil, over 6,800 apartment listings in Seoul disappeared within a week after the exemption ended. The decline was particularly rapid in non-Gangnam areas such as Guro District (-16.6%), Gangbuk District (-15.2%), and Seongbuk District (-14.1%). As the number of available properties decreased, buyers faced fewer options.

In a market where demand remains, a reduction in supply strengthens price support. In real estate, supply does not only refer to new apartment units but also includes existing listings. When taxes fail to motivate sellers and instead lock away listings, market supply diminishes. The government aimed to suppress demand, but in reality, a decrease in supply was the first outcome.

When taxes exceed the threshold that pressures sales, they become a mechanism that locks away listings. The recent rebound in Gangnam illustrates where that boundary lies.

This paradox is not new. The real estate policies of the Roh Moo-hyun and Moon Jae-in administrations were also subject to this cycle. Regulations aimed at suppressing demand reduced transactions, and the decrease in transactions increased scarcity—a pattern that has repeated itself. As regulations intensified, sellers had greater incentives to hold off. When taxes and loan regulations push demand out of the market, that demand does not disappear but rather lies dormant. The moment a small crack appears, prices return. The recent rebound in Gangnam occurred within that familiar cycle.

Gangnam was not a leader but a last bastion

More important than the fact that Gangnam prices have risen is that Gangnam was the last to do so.

For a long time, Gangnam has been a leading indicator in Seoul's real estate market. Prices in Gangnam would rise first, followed by Mapo, Yongsan, and Seongdong, and then the warmth would spread to the outskirts of Seoul and the metropolitan area. However, this time the order was different. Seoul moved first, and Gangnam joined last.

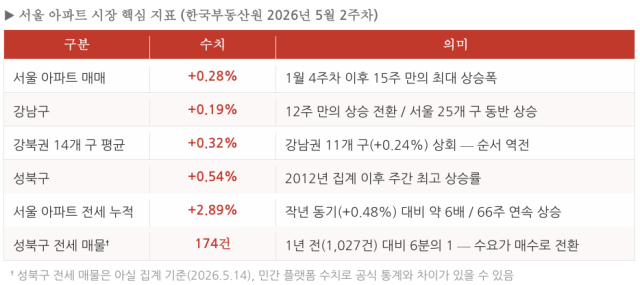

According to the Korea Real Estate Agency, the average increase in the 11 districts of Gangnam was 0.24%, while the average for the 14 districts in Gangbuk was 0.32%. Seongbuk District saw a 0.54% increase, and Jongno District recorded a 0.36% increase, marking the highest weekly rates since 2012. While Gangnam's 0.19% rise is notable, the speed of increases in Gangbuk and non-Gangnam areas is more significant. While Gangnam remained stagnant for 12 weeks, districts like Gangseo, Seongbuk, and Gwanak in non-Gangnam areas built momentum that exceeded the average for Seoul. While Gangnam was restrained, the upward pressure across Seoul remained uncontained.

This does not mean Gangnam has collapsed. On the contrary, it indicates that in this phase, Gangnam is not the starting point of the rise but rather the last line of defense. The fact that Gangnam has begun to move again suggests that the symbolic price level, which the government had been holding onto, is now shaking.

The rental market had already begun to signal this shift. According to Asil, the number of rental listings in Seongbuk District dropped to 174 on May 14, down from 1,027 a year ago, representing just one-sixth of the previous level. As rental listings decrease, tenants face fewer choices. They may have to accept higher rents, switch to monthly rentals, or return to purchasing homes.

This pressure has also affected the sales market. In Seongbuk District, the Gileum New Town 9 complex's 84㎡ units have repeatedly set new price records this year, indicating that buying interest in non-Gangnam areas has already begun to heat up. By the second week of May, apartment rental prices in Seoul had risen by 2.89%, continuing a 66-week streak of increases. This is not just a sales issue but a broader cost of living concern. While headlines have recently focused on Gangnam's price rise, the market had already been moving under the pressures of rental shortages and rising prices in non-Gangnam areas.

Demand for Gangnam cannot be explained solely by investment interest. It is a structural demand driven by factors such as school districts, proximity to workplaces, and expectations of redevelopment. Such demand does not disappear under tax pressures. When it remains outside of transactions, it can return to the market once price cracks appear. When regulations aimed at Gangnam reduce the number of properties available for sale, the scarcity of Gangnam increases. The number of buyers remains while the number of sellers decreases, creating a structural imbalance.

Concerns about supply also compound the situation. According to Real Estate R114, the number of new apartment units in Seoul is expected to drop from around 17,000 this year to about 8,000 by 2028. If tax changes were the direct trigger for Gangnam's rebound, the rental crisis and supply shortages have already been structural pressures pushing the market upward.

The warning left by Gangnam's May rebound

The May rebound in Gangnam is not just a simple price change over a week. It signals how taxes operate within the market. The government aimed to draw listings through taxation, but instead, the market saw a reduction in listings after the exemption ended. When taxes fail to change seller behavior, regulations tend to lock away supply rather than suppress demand.

The next variable is the tax reform in July. Strengthening property taxes for non-resident homeowners and reducing long-term holding tax exemptions are being discussed. However, the lesson from the current capital gains tax situation is clear. More important than imposing heavier taxes is ensuring that actual listings emerge. If sellers tilt their calculations back toward 'holding rather than selling,' the market is likely to respond in kind.

Taxes can be a tool to suppress housing prices. However, once they lock away listings, they become a mechanism that supports prices. The warning left by Gangnam's May rebound lies here: the critical factor is not the intensity of the tax but whether it draws sellers into the market or keeps them locked out.

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.