Is the Boom an Illusion?

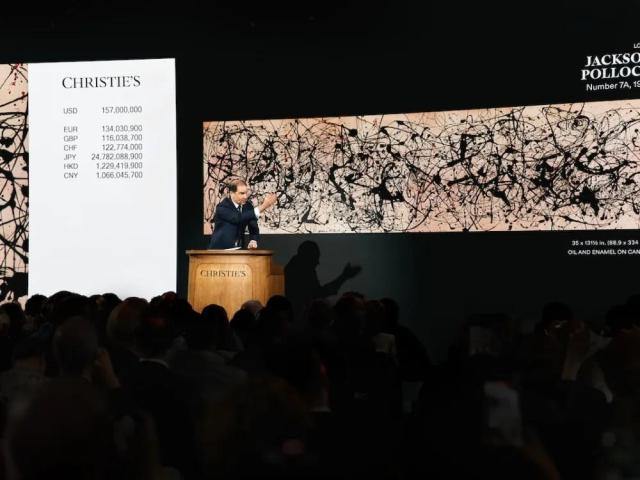

Recent reports of record-breaking auction sales in New York and London have created an illusion of a booming art market, with auction houses and art publications buzzing with excitement. Christie's and Sotheby's have garnered media attention by showcasing masterpieces that have generated billions in sales. However, a closer examination reveals that this surge is not indicative of a full market recovery but rather a localized rebound focused on ultra-high-value blue-chip artworks.Works by artists like Jackson Pollock have surpassed $180 million, while pieces by 20th-century masters such as Constantin Brâncuși and Mark Rothko continue to set new records. The names of Picasso, Mondrian, and Basquiat remain the most reliable guarantees in the auction world. This phenomenon is driven by a generational shift, as younger leaders from wealthy families take over, leading to the sale of collections from older collectors, resulting in record-breaking auction prices.

This trend reflects a typical pattern where funds gravitate toward established names and iconic works amid economic uncertainty. The U.S. market has capitalized on this trend, growing by over 25%, while China has seen a decline due to a real estate slump. The disparity among auction houses is also evident, with major players like Christie's and Sotheby's significantly increasing their revenues, while Phillips has reported a downturn, highlighting a growing polarization between top-tier and smaller auction houses.

The question remains about sustainability. After the baby boomer generation fades, will the next generation embrace works by Warhol or Rothko with the same passion? It is uncertain whether the rising prices of blue-chip artworks will hold post-generational transition. In response, some galleries are exploring new auction platforms to navigate this challenge, opting for 'technological innovation in sales methods' to avoid the structural crisis of overexpansion leading to bankruptcy.

The art market, currently in a deep slump, has seen wealthy collectors close their wallets, resulting in tedious negotiations over prices in private sales between galleries and collectors, diminishing the urgency to purchase artworks. Even exceptional pieces are increasingly left unattended as galleries take control of timelines to guide the market, which may be a necessary self-rescue strategy.

Self-Rescue Experiments in the Art Market

Recently, seasoned art dealers and market experts Dominique Lévy, Brett Gorvy, and Amalia Dayan have observed a growing share of one-on-one transactions at Christie's and Sotheby's. In 2025, private sales slightly decreased year-over-year, yet Christie's accounted for about 24% of total sales at $1.5 billion, while Sotheby's recorded approximately 17% at $1.2 billion. Phillips, however, saw a remarkable 66% increase in private sales, reaching around $200 million, underscoring the critical role of private sales in sustaining auction revenues.The trio, collaborating under the name Lévy Gorvy Dayan, launched a customized live auction platform called 'LGD Hammer' to enhance transparency in private transactions. This new platform directly addresses the issue of prolonged negotiations in artwork sales. By ingeniously combining traditional auctions and private sales, it allows for the auction of a single masterpiece or core collection on a designated day, facilitating live bidding via phone and online for top collectors worldwide. This approach maximizes focus and urgency, contrasting with the bulk offerings of major auction houses.

The auctioned artworks are first reserved at galleries for in-depth viewing, allowing ample time for research and appreciation before final pricing is determined through competitive bidding. This model not only facilitates sales but also provides a museum-quality experience and market tension. The distinctiveness of LGD Hammer stems from the founders' extensive auction experience. Having worked for decades at global auction houses like Christie's, they understand the essence of auctions better than anyone, internalizing the systems of major auction houses within galleries to combine the intimacy of private sales with the competitiveness of auctions. This is not merely a formal variation but a strategic attempt to address structural issues in the market.

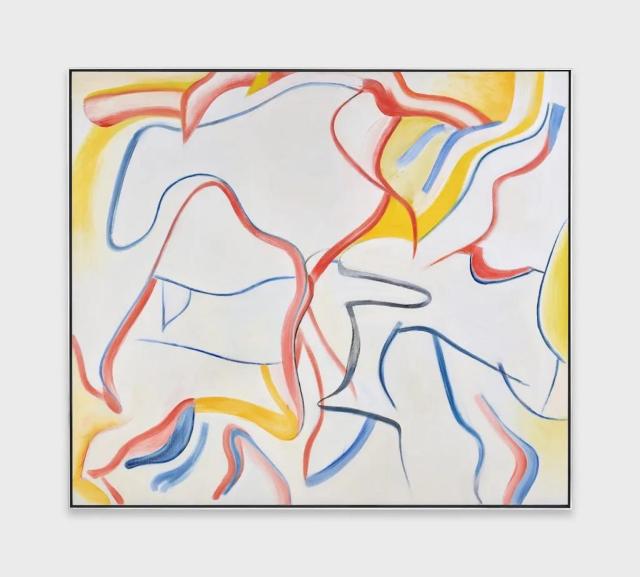

Ultimately, LGD Hammer represents an experiment to reinvigorate the art market, ensuring that artworks are no longer neglected and that collectors face pressure to make timely decisions. Whether this platform can break through the current market stagnation remains uncertain, but at the very least, it has reintroduced the essential elements of 'scarcity and competition' to art transactions. What is needed now is precisely this sense of urgency. LGD Hammer is a challenge to rekindle that spark. The first auction featured Willem de Kooning's Milkmaid, which sold within the estimated range of $10 million, validating the effectiveness of this new hybrid platform.

However, the mid-range market and emerging artists continue to struggle. Just a few years ago, the works of young artists, once driving speculative enthusiasm, have largely disappeared from auction houses. In major auctions at Sotheby's and Christie's, artists under 40 are few and far between, with Phillips featuring only one or two pieces. The energy that once characterized young artists, referred to as 'red chips,' has dissipated.

Consequently, the rise in average auction prices is solely attributed to high-value works, while the pieces by young artists have vanished from auction houses. The primary market, represented by galleries, faces increasing operational costs due to high rents and excessive fees for art fairs, leading to a loss of trust in the market. Many collectors hesitate to purchase artworks from galleries when pieces offered for tens of thousands of dollars sell for thousands at auction, highlighting the bubble in the primary market. However, some galleries that present high-quality new works at reasonable prices still see demand and sell out, indicating that the market is not entirely devoid of potential.

Recently, prominent galleries such as Blum Gallery, Venus Over Manhattan, and Clearing have faced liquidity crises due to soaring rental costs and exorbitant fees for international art fair booths, often relying on bank loans or external funding, which have led to closures.

Thus, while auction results may appear robust, they do not signify a comprehensive recovery of the art market. Instead, the market reveals a stark imbalance between the dazzling resurgence of blue chips and the stagnation of red chips. True recovery will only be possible when the flow of funds extends beyond ultra-high-value works to include emerging artists and mid-range priced pieces. The current activity is merely an illusion of prosperity, and a balanced ecosystem is crucial for a healthy future in the art market. The present art market is undergoing painful restructuring as it treats art more as an 'investment asset' than pure appreciation, leading to the deflation of an overheated bubble.

In fact, the recent closures of major galleries illustrate the structural limitations that often lead to sudden bankruptcies after a gradual decline. This current crisis results from galleries and auction houses approaching artworks solely as 'financial investment assets,' pushing their business models to their limits.

Major Auctions in May 2026

The unprecedented anomalies in the art market, characterized by unpredictable structural changes and a generational shift among collectors, are also evident in the Korean art market, particularly in the auction sector. The May auctions at Seoul Auction and K Auction lacked significant works that could drive the market. While international auction houses have drawn major collectors' works to boost sales, Korea's leading auction houses currently lack the capacity to do so.Nonetheless, the results from May auctions indicate a gradual movement in the Korean art market, albeit with cautious optimism. The market's response reflects selective reactions based on the types of artworks, price ranges, and artist recognition rather than a full recovery. K Auction saw 60 out of 77 lots sold, totaling approximately 7.2321 billion won, with a sell-through rate of 77.9%. The highest price at K Auction was Yayoi Kusama's Infinity Net (POWTY), 2014, which was estimated at 2.1 to 3.5 billion won but sold for the lower estimate of 2.1 billion won without significant competition. Seoul Auction recorded a sell-through rate of 69.8%, with total sales of about 5.66 billion won. Lee Ufan's Dialogue, 2018, estimated at 700 million to 1.2 billion won, started at 640 million won and sold for 1.04 billion won without much competition.

The auction results indicate that the blue-chip market remains central to the art scene. While works by established artists like Yayoi Kusama and Lee Ufan traded steadily, aggressive price increases were limited, suggesting that bidders are responding conservatively. This indicates that the market is operating around realistic pricing. In contrast, there were inexplicable strong competitions for relatively lower-priced works by young artists. Although these pieces have yet to be validated in the market, bidders exhibited a rather aggressive stance, indicating a need for further examination.

The works of Munassi (Kim Dae-hyun, 1980) attracted multiple bids in the mid-range, while Lee Mok-ha (1996) entered the high-price bracket in a short time, reflecting market expectations. However, such results do not necessarily indicate a healthy market. It is essential to scrutinize the structure of price formation and the conditions supporting those prices.

Seoul Auction's anticipated work, the colored manuscript of the Daedongyeojido, was unsold. This outcome highlights that the conditions for successful transactions are stringent, despite the significant academic value of cultural heritage works. It served as a reminder of the challenges in the high-end art market.

Ultimately, the key takeaway from this auction is not whether prices are rising but the credibility of those prices. A good market is one that can explain why high prices are achievable, rather than merely generating them. For the Korean art market to grow sustainably, it must go beyond viewing auction results as mere indicators of success and instead closely analyze and articulate the processes of price formation and the structures supporting those prices.

Therefore, we should view the May auction not merely as a sign of vitality but as an opportunity to assess the market's credibility. Balancing the stability of blue chips with the growth potential of young artists while ensuring the structural reliability of price formation is essential for the future of the Korean art market.

From Survival to Solidarity: Restructuring the Art Market

The era of large galleries in the West is waning, and the same is true for several major galleries in Korea. The previous strategy of international mega-galleries focusing on hardware expansion by increasing locations has proven unsustainable. With the global economic downturn, high exchange rates, and a speculative market centered on ultra-high-value works cooling off, galleries are seeking new paths through mergers and collaborations to reduce fixed costs and diversify risks. The era of individual survival is giving way to one of solidarity.Voluntary mergers and the emergence of mega platforms are notable trends. Smaller galleries, feeling the limitations of independent operations, are being absorbed into larger gallery networks, while capital-rich mega-galleries are acquiring promising mid-sized galleries to expand their artist portfolios. This is not merely a survival strategy but a reflection of structural changes in the market. Additionally, the approach to international expansion is changing. Instead of costly standalone locations, 'hybrid spaces' are emerging, where local galleries share costs and risks by operating joint spaces. The establishment of a joint location in Hannam-dong, Seoul, by Berlin's Meyer Riegger and Paris's Jocelyn Wolff exemplifies a new approach to the Asian market. At art fairs, 'booth sharing' has become commonplace, with galleries collaborating to share costs and cross-promote artists.

This restructuring period has left deep scars on the Korean art market. The inflated transaction record of 1 trillion won in 2022, aimed at quantitative expansion, has proven to be a mirage, as the market that once thrived is now facing a painful period of deflation and consolidation due to the global recession and high exchange rates.

With estimates suggesting that over 100 small galleries have closed in the past four years, the current crisis is not merely a retreat but a process of improving the market's structure. The decline in speculative purchases of ultra-high-value works and the increasing attention on mid-range pieces priced between 100 million and 500 million won, as well as conceptually rich works, further support this shift.

As Western mega-galleries withdraw from Frieze Seoul, Asian galleries are stepping in, transforming Seoul from a 'sales hub for Western art' to an 'Asian hub platform.' This shift is crucial, and those responsible for strategizing and responding to these changes in Korea must not remain passive, merely waiting for opportunities. The Ministry of Culture, Sports and Tourism's approach to the art market, treating it from a cultural industry perspective rather than establishing comprehensive plans for visual arts promotion, is problematic. Furthermore, policies proposed by civil servants with limited understanding of the art market, often based on a two- to three-year rotation, are unlikely to yield effective results beyond mere financial distributions. The execution of these policies by the Arts Management Support Center, staffed by individuals lacking experience in the art market, further highlights the absence of appropriate policies for the Korean art market.

In reality, Korean collectors are moving away from 'blind investments' toward practical collecting, seeking works by Korean artists with historical depth. Ultimately, the current crisis is not merely a downturn but a turning point toward a new order. The era of individual survival has ended. Through solidarity and collaboration, the market will revive. The Korean art market must undergo painful restructuring to move toward a stronger and more sustainable future.

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.