The inflation shock unleashed by the monthslong Strait of Hormuz blockade is still working its way through central bank decisions, reviving upward pressure on interest rates and the U.S. dollar across Asian financial markets.

The Bank of Japan and the European Central Bank have already tightened policy. The Bank of Korea may be next in July. The U.S. Federal Reserve on Thursday signaled that it could soon join them.

Washington and Tehran signed a provisional agreement aimed at restoring traffic through the Strait of Hormuz and easing U.S. sanctions on Iranian oil.

Oil prices reacted immediately. Brent crude fell to $77.41 a barrel and U.S. West Texas Intermediate to $74.43, both their lowest levels since early March, as markets priced in the return of Middle Eastern supply.

But the agreement is not a peace treaty.

It is a 14-point memorandum built around a 60-day negotiating period, leaving major issues unresolved, including Iran's nuclear program, sanctions relief and the long-term rules governing passage through the strait.

Even if toll-free navigation is temporarily restored, transit terms could become a new source of friction once the two-month window expires.

The agreement aims to normalize shipping within 30 days. Yet many shipowners may wait for clearer signs that the deal will hold before returning vessels, suggesting that supply chains could take longer to recover.

The economic damage, meanwhile, has already been done.

When fears of a Hormuz blockade peaked in March, Dubai crude surged to around $130 a barrel. South Korea was particularly exposed, with roughly 70 percent of its crude imports dependent on the strait.

The resulting shock to prices, logistics and monetary policy has yet to fully run its course.

The Fed's latest meeting illustrated how those effects are now feeding into policy decisions.

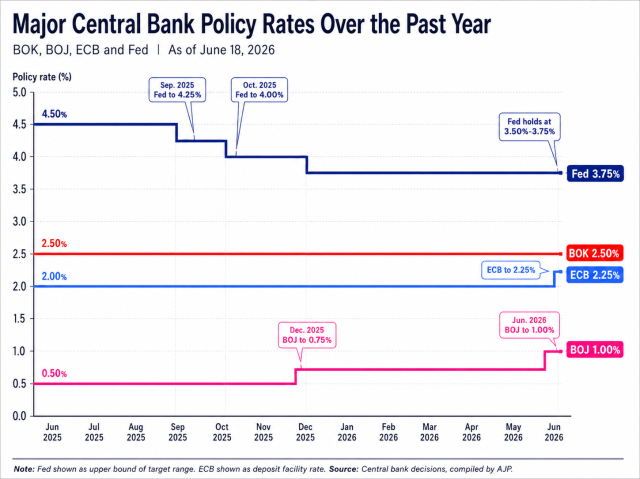

The Fed kept its benchmark rate unchanged at 3.50 percent to 3.75 percent after its June 16-17 meeting. The decision, however, was far from dovish.

The stronger signal came from the dot plot.

The median estimate for the federal funds rate at the end of this year rose to 3.8 percent from 3.4 percent in March. Of the 18 officials who submitted projections, nine now expect at least one additional rate increase this year. Fed Chair Kevin Warsh did not submit his own forecast.

Warsh reinforced the message at his first post-meeting press conference, saying no rate cut was discussed. He noted that inflation had remained above the Fed's 2 percent target for more than five years and reiterated the central bank's commitment to restoring price stability.

The Fed also adopted a more hawkish tone, removing forward-guidance language on future policy adjustments and citing supply shocks, including energy, as a source of persistent inflation.

Markets reacted immediately.

The two-year Treasury yield rose 13 basis points to 4.18 percent, while the 10-year yield climbed 5 basis points to 4.49 percent. The dollar index gained 0.9 percent to 100.39, moving back above the 100 mark, while the S&P 500 fell 1.2 percent to 7,420.

For Asia, however, the picture is more complicated than simply cheaper oil.

Lower energy prices improve trade balances and ease pressure on households. But a stronger dollar weakens local currencies, tightens financial conditions and raises import costs.

For Asian central banks, the U.S.-Iran agreement has therefore shifted, rather than eliminated, the source of inflation pressure. The focus is moving from oil itself to interest rates and exchange rates, while the effects of the Hormuz shock continue to filter through monetary policy.

The BOJ this week raised its policy rate to 1.0 percent from 0.75 percent, taking rates above 1 percent for the first time in 31 years. The ECB raised its deposit rate to 2.25 percent last week.

Senior Deputy Governor Ryoo Sang-dai said Thursday that the Fed, following tightening by the ECB and BOJ, had pointed to the possibility of further policy adjustments in response to inflation pressures, suggesting a broader shift among major central banks.

A day earlier, Governor Shin Hyun-song personally laid out the case for inflation remaining elevated "for a considerable period," projecting headline inflation to hover around 3 percent in the second half of the year.

He said the surge in fuel prices would continue to have a lagged effect even after oil returned to prewar levels, while the exchange rate remained near crisis-period levels. He also warned that rising income from record semiconductor earnings and stock market gains could build additional demand-side inflation pressure.

The remarks amounted to an early warning ahead of July's rate-setting meeting.

Local market moves explain policymakers' caution.

The won strengthened to 1,513 per dollar on June 17 from 1,539 on June 5, while the three-year government bond yield fell to 3.71 percent from 3.88 percent.

Cheaper oil helps inflation and the trade balance, but a stronger dollar works in the opposite direction by raising import prices and bond yields while weakening the currency.

If the Fed's tightening bias persists, that pressure will only intensify.

For Asian markets, the risk is that the U.S.-Iran memorandum arrived too late to revive the old rate-cut narrative.

The inflation shock triggered by the Hormuz blockade has already pushed the world's major central banks back toward tightening.

Copyright ⓒ Aju Press All rights reserved.