SEOUL, June 24 (AJP) -Higher interest rates could help cool leveraged bets on stocks and property, but they would also increase burdens on households and create fresh financial risks, the Bank of Korea warned on Wednesday, as senior officials continued to signal that the benchmark rate would rise from the current 2.50 percent.

In its June Financial Stability Report, the central bank said Korea’s financial system remains broadly stable, supported by stronger economic growth, resilient financial institutions and sound external payment capacity.

But the report pointed to a growing policy dilemma as financial and foreign exchange markets become more volatile, housing prices in Seoul and surrounding areas rise again, and investors take on more leverage to chase asset gains.

The BOK, which has kept its base rate at 2.50 percent since last cut in May last year, judged that rates would need to be raised “at an appropriate time” after weighing inflation pressure, economic conditions and financial stability risks.

In a separate analysis, the central bank said higher market rates could help ease financial imbalances by restraining debt-funded asset investment and reducing the risk of further asset-price gains.

Jang Jeong-su, deputy governor of the BOK, said at a press briefing that rate hikes could help reduce medium- to long-term financial instability.

The effect, however, would not be one-sided, he said.

“Rate hikes can lower volatility and vulnerabilities in real estate and stock markets, but they can also increase the burden on vulnerable borrowers,” Jang said.

The BOK’s Financial Stress Index, which measures short-term stress, stood at 17.2 in May, remaining in the cautionary zone. The Financial Vulnerability Index, which tracks medium- to long-term vulnerabilities, rose to 46.0 in the first quarter, slightly above its long-term average of 45.7.

Lim Kwang-kyu, director general of the BOK’s Financial Stability Department, said the FSI is a coincident indicator of short-term stress, while the FVI shows how much financial instability has accumulated over a longer horizon.

He said the FSI had risen during the Middle East crisis before easing recently, but added that both indicators remain in the cautionary zone and require close monitoring.

Household debt remains one of the central bank’s biggest concerns.

Jang said Korea’s high household debt ratio is a problem the economy still needs to solve, although the ratio could decline if nominal gross domestic product continues to grow.

But he cautioned that recent nominal GDP growth has been concentrated in specific sectors, making it difficult to view the improvement as broad-based.

“Given the steep rise in property prices, we need to stay alert to household debt risks,” he said.

Household credit stood at 1,993.1 trillion won at the end of the first quarter, up 3.5 percent from a year earlier.

The household debt-to-disposable-income ratio fell to 134.1 percent from 139.7 percent at the end of the third quarter last year, but the share of vulnerable borrowers rose to 6.7 percent by number of borrowers from 6.4 percent over the same period.

Household loan growth has also accelerated again. Monthly household loans increased by an average of 2.7 trillion won in the fourth quarter of last year and 3 trillion won in the first quarter, before rising by 3.5 trillion won in April and 9.3 trillion won in May.

The BOK said housing transactions ahead of the end of temporary tax relief for multiple-home owners were reflected in loans with a lag, while other loans, including borrowing linked to stock investment, also increased.

The central bank warned that the stabilizing effect of higher lending rates could be weakened if profit-taking from the stock market flows into housing.

If demand for homes in non-regulated areas strengthens amid rising lease prices, household debt growth could pick up again, the BOK said, calling for consistent management of expectations for further home-price gains.

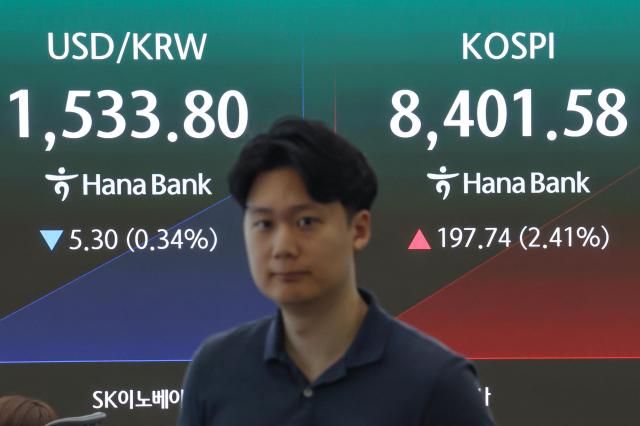

Leveraged stock investment has emerged as another risk, with the rapid rise in Korean stocks compared with major overseas markets appearing to be a key driver, Jang said.

“It is true that there are concerns about external effects, where even investors who did not borrow to invest could suffer losses from forced selling,” he said, adding that the BOK would continue to consult with relevant authorities.

Asked about recent swings in the KOSPI, Jang said it was difficult to predict whether foreign selling pressure had fully run its course. “If the market rises sharply in a short period, it could again trigger foreign selling,” he said.

Foreign investors pulled a net $83.37 billion from Korean securities from January through June 9. Stock investment posted a net outflow of $94.81 billion, while bond investment recorded a net inflow of $11.44 billion.

The BOK said the won-dollar exchange rate rose with high volatility due to Middle East-related geopolitical risks and foreign selling of Korean stocks, but foreign currency funding conditions remained broadly favorable and Korea’s external payment capacity stayed strong.

Jang said Korea’s failure to be added to MSCI’s developed-market watch list does not erase the progress made in market reforms, saying MSCI has viewed Korea’s reform efforts positively. He said continued work to extend foreign exchange trading hours and establish an offshore won settlement system could eventually lead to inclusion.

Hwang Kun-il, the Monetary Policy Board member who oversaw the preparation of the report, said in a separate message that risks from vulnerable sectors, market volatility, rising home prices and leveraged asset investment require continued attention.

Copyright ⓒ Aju Press All rights reserved.