On July 7, the Financial Services Commission (FSC) and the Korea Exchange announced they would begin soliciting opinions on proposed amendments to the Korea Exchange regulations and guidelines regarding dual listings, which include a principle of prohibition with exceptions. The consultation period will last until July 14, after which the proposals will be finalized following approval from the Securities and Futures Commission and the FSC.

This initiative is a follow-up to the 'Capital Market Improvement Plan' announced in March. The FSC has noted that dual listings have been pursued in practice despite concerns over infringement of common shareholder rights, particularly in comparison to international norms. As of the end of last year, the ratio of market capitalization held by listed companies in relation to total market capitalization was 11.2% in South Korea, significantly higher than in the United States (0.05%), Japan (4.0%), China (2.4%), and Taiwan (2.7%).

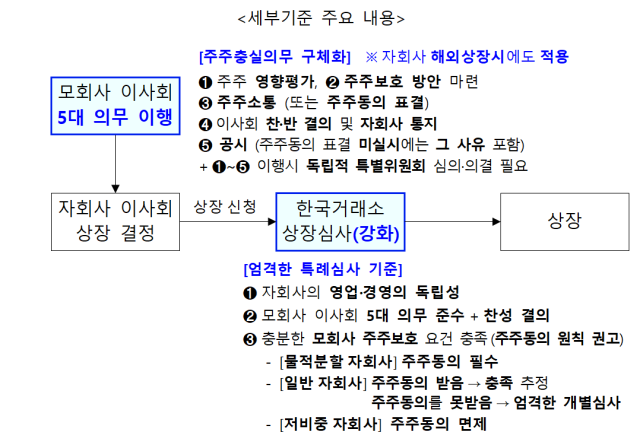

The new standards will apply when a parent company, already listed, seeks to list a non-listed subsidiary that it effectively controls. This includes subsidiaries defined under the External Audit Act and those in a vertical control relationship under the Fair Trade Act.

The parent company board will be subject to five key obligations that clarify the duty of loyalty to shareholders under corporate law. They must assess the impact of dual listings on shareholders, develop protective measures such as stock dividends or share buybacks, communicate with shareholders, and confirm shareholder consent when necessary. The board must also notify the subsidiary of the results following a vote, and the process must be disclosed in stages. If shareholder consent is not obtained, the reasons must also be disclosed.

Shareholder consent is generally recommended, but subsidiaries created through physical division must obtain it. For general subsidiaries, obtaining consent will be presumed to meet the requirements for shareholder protection, while those that do not obtain consent will undergo individual assessments to determine the level of investor protection.

The criteria for shareholder consent will apply the '3% rule' used for appointing audit committee members under corporate law. Major shareholders cannot exercise voting rights exceeding 3%, and consent must be obtained from a majority of attending voting rights and at least one-fourth of total voting rights.

Conversely, subsidiaries with revenues, operating profits, and assets all less than 10% of the parent company will generally be exempt from requiring shareholder consent. However, if all three indicators are below 10% but the subsidiary is recognized as significant based on expected corporate value, it will be excluded from the exemption.

The FSC stated, "The entities best positioned to assess whether the rights of common shareholders in the parent company are being infringed are the parent company's board and its shareholders. Therefore, we designed the system so that they first evaluate the appropriateness of dual listings, and the exchange respects this in the final review."

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.