This is the first installment of AJP's Chip Republic series, examining how South Korea is reshaping its industrial landscape around semiconductors and artificial intelligence.

SEOUL, July 15 (AJP) - South Korea has rarely drawn as much scrutiny as it does now, as it emerges as the epicenter of the memory chips fueling the AI industrial revolution.

Two companies — Samsung Electronics and SK hynix — account for roughly 40 percent of the country's record exports and main stock market, and are helping drive what could be South Korea's fastest nominal economic growth in three decades.

They are also behind eight out of 10 core chips fueling the AI wave. That windfall is now financing an unprecedented national push to expand the so-called "chip republic."

Samsung and SK hynix were already ramping up capacity before this year's AI-driven surge in demand.

Now both are planning trillions of dollars in additional investment across their home turf, extending the country's semiconductor heartland well beyond its traditional production base as they aspire to maintain global supremacy over the brain behind AI power.

The astronomical scale of the buildout, nevertheless, raises hard questions about infrastructure, financing, and most of all, whether global demand will stay strong long enough to fill the factories being built for it.

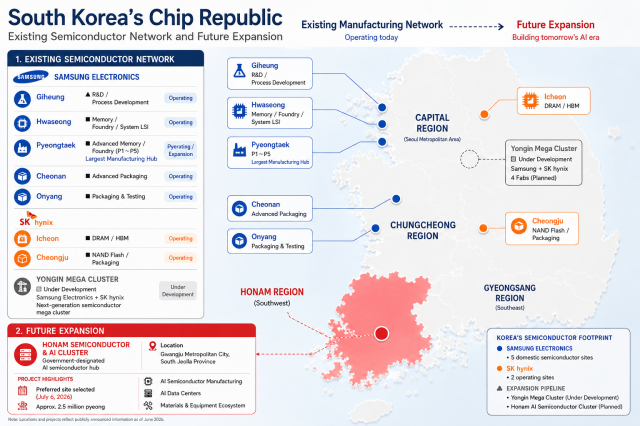

South Korea's semiconductor belt — long concentrated in an industrial corridor south of Seoul — is expanding into a nationwide network of fabrication plants, packaging facilities, suppliers, and new urban infrastructure, as the country makes its biggest-ever bet on artificial intelligence.

From Samsung's existing operations in Giheung, Hwaseong, and Pyeongtaek to new production planned in Yongin, Cheongju, and the industrially-neglected southwest, the expansion is redrawing the geography of South Korea's most important export industry.

The mega-projects

On June 29, the government unveiled three national "mega-projects" spanning semiconductors, physical AI, and AI data centers, pledging faster approvals and infrastructure support to secure South Korea's position in what officials describe as the next industrial cycle.

"We must secure the core elements of AI faster than any other country," President Lee Jae Myung said at the announcement.

The semiconductor portion alone calls for Samsung and SK hynix to build four large fabrication plants in the southwest called Honam — two each — at a combined projected cost of 800 trillion won ($518 billion).

The government said it would partner with the companies from land acquisition and approvals through construction, while building out a surrounding ecosystem of suppliers and skilled labor.

A further 81 trillion won is earmarked for the central Chungcheong region, including new high-bandwidth memory (HBM) production in Cheonan and Onyang and HBM packaging capacity in Cheongju. The southeast and Daegu-Gyeongbuk regions are meant to develop as hubs for materials, parts, and equipment supporting the broader expansion.

Taken together, the plans amount to an attempt to push semiconductor manufacturing beyond the Seoul metropolitan area and establish a second major production base in the southwest.

A decade-long bet, not a single check

The numbers are difficult to compare with a conventional corporate capital budget.

Samsung has outlined 2,450 trillion won ($1.6 trillion) in South Korean investment through 2040, including 2,100 trillion won across its Pyeongtaek and Yongin clusters, 400 trillion won for fabs in Gwangju, and 56 trillion won for HBM facilities in Cheonan and Onyang.

SK hynix has laid out a separate 1,100 trillion won framework: 600 trillion won for Yongin, 100 trillion won for Cheongju, and 400 trillion won for the southwest.

SK hynix envisions four new fabs and Samsung six, with completion pulled forward to 2033 from an original 2045 target; SK hynix's first new fab could open as early as next year. Each plant is estimated to cost roughly $30 billion.

These figures shouldn't be read as money being spent immediately or all at once. The programs run across different timeframes, include projects at very different stages of maturity, and remain contingent on future board approvals, chip demand, and infrastructure readiness.

"Our roadmap is contingent on market conditions and other factors," SK hynix Chairman Chey Tae-won said at a joint press conference with President Lee and Samsung Electronics Chairman Jay Y. Lee.

The scale of the announced spending has itself become a source of concern: investors worry the market may not be large enough to absorb all the new capacity by the time it comes online, and KOSPI chip stocks have slid in recent weeks on glut fears.

The investment blueprints, taken as a whole, describe an industrial buildout stretching well over a decade — not a single committed round of spending.

From a chip corridor to a nationwide network

Samsung's domestic manufacturing footprint already spans several cities in Gyeonggi Province. Its 2025 business report lists Suwon, Gumi, Gwangju, Giheung, Hwaseong, and Pyeongtaek among its principal domestic sites. Its Device Solutions division produces DRAM and NAND flash memory, mobile application processors, and other chips, while its foundry business manufactures designs for outside customers across three main lines: memory, System LSI, and foundry.

Giheung has long served as Samsung's semiconductor base and now also hosts a next-generation R&D complex. Hwaseong houses memory, System LSI, and foundry operations together, while Pyeongtaek has become the company's largest production site. Yongin is meant to become another major manufacturing hub as Samsung accelerates construction of its first fab there.

Semiconductors are already Samsung Electronics' core earnings engine: the Device Solutions division generated 130.13 trillion won in sales in 2025, up 17.2 percent year-on-year, with operating profit rising 64.7 percent to 24.86 trillion won — 57 percent of Samsung's total operating profit across all divisions before intersegment adjustments.

Those results rest on a string of technology milestones: mass production of sixth-generation 10-nanometer-class DRAM began in 2025, following the industry's first ninth-generation V-NAND in 2024 and the world's first 3-nanometer gate-all-around foundry chips in 2022.

The new factories aren't chiefly about adding commodity volume — they're built to meet growing demand for HBM and other high-value memory used alongside AI accelerators, as well as advanced foundry and packaging capacity.

SK hynix's network follows a related but distinct path. Its established operations are based in Icheon and Cheongju, while its new Yongin cluster is planned as a four-fab complex, with the fourth fab targeted for completion by 2033 — though timing and scale remain subject to market and board decisions.

SK hynix has become central to the AI boom through its position in HBM, the stacked memory used with GPUs and AI accelerators. CEO Kwak Noh-jung said this month that memory demand could outstrip supply beyond 2030, with the shortage potentially most acute in 2027 — despite aggressive expansion across the industry.

That outlook captures the logic behind the government's strategy: even the fabs already under construction may not be enough if AI infrastructure spending keeps pace.

An AI boom becomes industrial policy

For South Korea, this investment drive is not simply a matter of corporate capacity planning — it has become national economic strategy.

Semiconductors have grown increasingly central to the country's exports and growth as global AI-server spending lifts memory demand. According to preliminary Korea Customs Service data, semiconductor exports surged 188.4 percent year-on-year in the first 20 days of June, accounting for 41.2 percent of total exports.

On July 14, the government raised its 2026 growth forecast to 3.0 percent from 2.0 percent, citing stronger semiconductor exports and AI-related demand, and framed the three mega-projects as part of a broader push to lift the economy's potential growth rate.

The boom has also strengthened both chipmakers' balance sheets. Samsung's DS division added nearly 9.8 trillion won in operating profit year-on-year in its 2025 report, reflecting a sharp recovery in its semiconductor business.

At the June 29 briefing, Samsung Chairman Lee framed the expansion as a partnership between industry and the state: "I am confident that if companies, the government and local governments join forces, we can build an irreplaceable South Korea." SK Group Chairman Chey struck a similarly bold note: "The future of AI will be built in South Korea."

The ambition here goes beyond simply defending South Korea's position as the world's leading memory producer.

The goal is to link semiconductor manufacturing with AI data centers, robotics, advanced packaging, and materials and equipment supply chains across multiple regions — and that scale is also the project's central risk. Today's cash flow, export growth, and factory utilization are being carried by an exceptional AI-driven memory cycle.

The new plants, however, will operate across several future cycles, in which today's shortages can turn into tomorrow's oversupply, and high prices can fall just as sharply as they rose.

That tension — between the urgency to build and the danger of building too much — will decide whether South Korea's semiconductor empire becomes the backbone of the global AI economy, or another costly monument to the industry's volatility.

The infrastructure behind the fabs

Before a single wafer can move through a new production line, an entire industrial system has to be built around it.

Semiconductor plants require enormous, continuous supplies of electricity and ultrapure water, along with roads, transmission networks, wastewater treatment, industrial gas supply, and housing for tens of thousands of workers and contractors — making the government's chip strategy as much an infrastructure project as a technology policy.

At a follow-up meeting on July 6, President Lee and government and corporate officials reviewed land, power, and water requirements for the new southwestern cluster and ways to speed up investment in Yongin.

The presidential office said it would set up a dedicated coordinating body and hold monthly public-private reviews to clear delays across ministries and local governments.

Presidential Chief of Staff Kang Hoon-sik said regulatory approvals should move fast enough that companies experience the process as "super fast," warning that strategic investments could not afford to get buried in paperwork.

That urgency reflects a basic constraint: a chipmaker can design a fab and order equipment, but it can't build national-scale infrastructure on its own.

In Yongin, where Samsung and SK hynix are each pursuing separate mega-clusters, the challenge is already visible.

SK hynix's Wonsam complex is designed for four fabrication plants; the first phase of its industrial water system is meant to deliver 265,000 tonnes a day through a 36.8-kilometer pipeline linking the site to the Han River system, according to the Yongin city government.

Power infrastructure, including new substations, is being built on a parallel timeline. Yongin Mayor Lee Sang-il said in January that water and power facilities for the SK hynix complex should be finished in the second half of 2026, with part of the first fab's clean room ready for equipment installation in the first half of 2027.

Those schedules matter because clean rooms need tightly controlled temperature, humidity, vibration, and particle levels — they can't simply be installed in an unfinished shell — while power disruptions can damage work in progress and force lengthy recalibration. For the national strategy to work, infrastructure has to move alongside, and in some cases ahead of, the factories themselves.

The government has pledged to support the southwestern base from site acquisition through construction, and plans to build out the southeast and Daegu-Gyeongbuk as materials and equipment hubs, and Chungcheong as a packaging center through the planned 81 trillion won investment.

The intent is to prevent the expansion from becoming a scatter of isolated plants: a modern semiconductor cluster needs equipment makers, chemical suppliers, maintenance contractors, and research labs operating near the major fabs, and delays anywhere in that network can ripple into production schedules at facilities costing tens of billions of dollars apiece.

The state is also trying to correct the industry's geographic concentration. The existing heartland runs largely through Gyeonggi Province — Samsung's Giheung, Hwaseong, and Pyeongtaek sites, SK hynix's Icheon operations, and the emerging Yongin clusters. The new southwestern complex is meant to become a genuine second manufacturing base, with regional packages covering financing, regulatory exemptions, technology, taxation, labor, and infrastructure.

There's an economic logic to that beyond regional balance: clustering multiple fabs in one area attracts suppliers, builds specialized labor markets, and shortens delivery times for equipment and materials.

But replicating that ecosystem in a new region is expensive and slow, particularly while most experienced engineers and suppliers remain concentrated around existing campuses.

The factories may well rise faster than the communities needed to run them.

A nation built around two chipmakers

Korea's semiconductor strategy hinges on Samsung and SK hynix — both its greatest strength and its clearest vulnerability. Between them, the two companies dominate global memory production and hold the financial capacity, technical expertise, and customer relationships needed to build at the scale the government envisions.

That concentration cuts both ways. New fabs take years to plan, build, and equip — waiting until a shortage becomes acute risks bringing new supply online only after the strongest part of the cycle has passed. But building ahead of demand carries the opposite risk.

Memory chips have long been among tech's most cyclical products: tight supply and high prices spur expansion, only for the new capacity to arrive as demand cools, dragging down prices, profits, and capital spending across the industry.

The current round of investment dwarfs previous expansion cycles — and that scale is the real story behind the headline numbers. These figures represent the outer edge of a long-term industrial blueprint, not capital already committed to construction contracts; individual fabs still require company-level approval, and equipment orders will depend on demand projections as each line nears completion.

The government's preferred timetable may also not match the companies': for policymakers, moving fast secures regional investment and strengthens South Korea's place in the AI supply chain; for the chipmakers, preserving the option to slow or redirect spending is essential in an industry where a single shift in customer orders can erase billions in expected revenue.

"We're readying the firepower, but nobody knows how long this boom will last, and what the future beholds," said a Samsung Electronics official, underscoring the inner anxiety as the company takes unprecedented steps.

Underinvestment carries its own risks — HBM and advanced DRAM are more complex to produce and consume more capacity than conventional memory, and supply could stay constrained even as spending rises if AI data-center demand keeps growing at its current pace.

But the further the forecasts stretch beyond 2030, the wider the range of plausible outcomes becomes.

Samsung and SK face different tests

Although Samsung Electronics and SK hynix are investing under the same national strategy, they face different commercial challenges.

SK hynix enters the expansion from a position of strength after establishing a dominant position in high-bandwidth memory, the AI-focused chips that have fueled record profits and enabled the company to raise $26.5 billion through its U.S. share offering. Its challenge will be financing and executing one of the industry's largest long-term investment programs without overextending itself if market conditions change.

Samsung faces a different test. As the broader semiconductor company, spanning memory, foundry and logic chips, it has more opportunities to benefit from AI demand but also greater competitive pressures. Its massive domestic investment will ultimately depend not only on overall memory demand but also on whether it can regain momentum in advanced HBM and translate new manufacturing capacity into profitable production.

Korea's semiconductor strategy is no longer simply about building more chip factories. It is an attempt to redesign an industrial economy around artificial intelligence by linking memory production, advanced packaging, AI data centers, robotics and regional manufacturing into a single national strategy.

That ambition also represents the project's greatest risk. The extraordinary cash flow now funding the expansion is being generated by an exceptional AI-driven memory boom, while the factories being planned today will operate across multiple market cycles over the next two decades.

Whether Korea's "Chip Republic" becomes the backbone of the global AI economy—or another reminder of the semiconductor industry's boom-and-bust nature—will depend less on how many fabs are built than on whether global AI demand remains strong enough to keep them competitive long after today's surge has faded.

The government has framed the expansion as a way to spread the benefits of advanced industry more evenly across the country. President Lee has said the gains from semiconductors and AI should reach people nationwide, and the presidential office has described the mega-projects as a shift away from growth concentrated in the capital region.

But semiconductor clusters don't automatically produce balanced development.

Large fabs generate construction demand, raise local tax revenue, and draw suppliers into surrounding industrial zones; they also lift housing demand and create business for restaurants, transport operators, and retailers.

The higher-value parts of the ecosystem, though, tend to stay concentrated among major corporations, specialized contractors, and highly trained engineers — smaller local businesses may see more foot traffic without gaining real access to the core technology and procurement networks that generate the largest returns.

Whether the new southwestern project can reproduce those benefits at scale will depend on the quality of jobs created, how many suppliers actually relocate, and whether local governments can build schools, housing, and transport ahead of population growth rather than scrambling to catch up.

It will also depend on whether the factories stay fully utilized once built: a fab running near capacity can anchor a regional economy for decades, while one that's delayed, scaled back, or run under capacity has a very different impact — regardless of how large its original investment announcement was.

The geographic expansion is also likely to intensify competition for skilled labor. Samsung and SK hynix already recruit from the same pool of semiconductor engineers, equipment specialists, and graduates; adding fabs in Yongin, Cheongju, and the southwest will only increase demand across production, maintenance, process engineering, and facility management.

Training programs can expand quickly — experienced personnel can't be produced on the same timetable as buildings.

That leaves the government's regional strategy facing a circular problem: companies want to invest where infrastructure and talent already exist, but new regions can't build those ecosystems without first attracting large corporate investment.

That makes the first wave of fabs especially consequential — their construction and early operation will determine whether suppliers and workers come to see the new regions as durable industrial centers, or simply as extensions of clusters still anchored elsewhere.

Though both companies are investing under the same national strategy, their commercial positions diverge sharply.

SK hynix enters this buildout from a position of real strength in HBM. Its early bet on stacked memory paid off as AI accelerator demand surged, turning what was once a niche product into one of the most valuable components in the semiconductor market — driving record profits, a soaring market value, and easier access to capital.

Its risk lies in the sheer scale now expected of it: 600 trillion won for Yongin, 100 trillion won for Cheongju, and 400 trillion won for the southwest. Even after the U.S. offering, that program may require additional financing structures, including partnerships or joint ventures.

Samsung faces a different set of questions. As the broader company — spanning DRAM, NAND, logic-chip design, and foundry — it has more ways to capture AI-driven demand, but also has to allocate capital across businesses with very different competitive positions.

It's been working to regain ground in advanced HBM while improving yields and customer traction in foundry, so the payoff from its large-scale domestic investment will hinge not just on overall memory demand but on whether it can convert new capacity into competitively priced, qualified products.

Accelerating construction could help Samsung close a capacity gap — but it also raises execution risk if infrastructure, equipment installation, and customer qualification don't advance in step.

The national strategy ultimately rests on two distinct corporate bets: that SK hynix can scale its AI-memory lead without overstretching its finances, and that Samsung can turn its manufacturing scale into renewed competitiveness across advanced memory and foundry.

South Korea's semiconductor strategy is no longer about individual factories. It's an attempt to redesign an industrial nation around artificial intelligence — and whether that ambition succeeds will depend not on how many factories get built, but on whether they stay competitive long after today's AI boom has faded.

Copyright ⓒ Aju Press All rights reserved.