South Korea’s payment gateway (PG) industry is expanding rapidly, but about seven in 10 fintech companies are operating without registering as an electronic financial business, a new survey found. Despite tighter oversight of PG operators, many firms still take part in payment functions outside the regulatory system, raising concerns about blind spots in supervision.

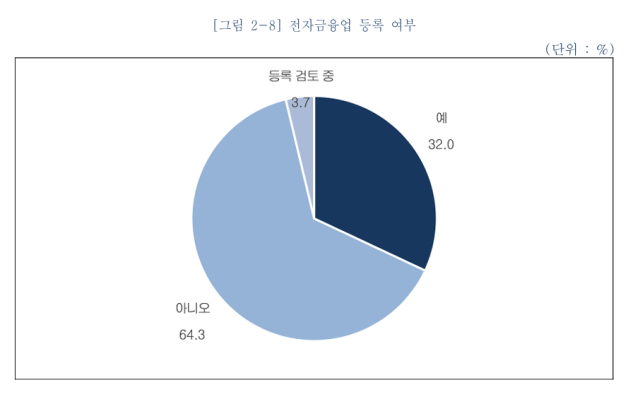

According to the Korea Fintech Industry Association’s “2025 Fintech Industry Survey,” released Monday, only 32% of 322 surveyed fintech companies were registered as electronic financial businesses. Another 64.3% were operating without registration, and 3.7% said they were considering registering. The association said this was the first time results of a full survey on fintech firms’ registration status had been made public. The survey covered a wide range of fintech fields — including payments, wealth management, insurtech and IT and solution providers — so the unregistered share does not necessarily equal the unregistered share among firms that are required to register.

Under the Electronic Financial Transactions Act, businesses that provide services such as simple payments, prepaid top-ups and settlement must register with financial authorities. Operating without registration can be punished by up to three years in prison or a fine of up to 20 million won. Critics have said the law’s narrow definition of PG business leaves gaps, including for “dual-business” PG operators that run their main business — such as online marketplace brokerage — while also handling settlements as a side activity.

Industry officials also argue that registration requirements — including capital, staffing and security systems — can be a high barrier for early-stage startups. Some companies say they only provide technology and do not directly control the flow of funds, and therefore interpret themselves as not subject to registration.

Registration rates varied sharply by industry. Financial-sector firms, which have traditionally provided financial functions, showed a 59.2% registration rate. By contrast, information and communications firms and software/IT firms posted rates of 13.9% and 20.5%, respectively. The report attributed this in part to IT-based companies defining their services as “technology services” while in practice performing PG-like functions such as accepting payments or handling settlements without registering.

The report warned that as platform-based payment ecosystems expand, more businesses are becoming involved in payment and settlement processes while remaining outside the scope of electronic financial business registration, increasing the risk of consumer harm.

On some online platforms, consumers may feel they are paying through the platform itself, but settlements are often handled by a separate PG firm or financial institution. When payment delays or refund disputes arise, users may struggle to identify who is responsible, delaying relief, the report said.

The report also found growth in “PG-like” firms that remain outside regulation, particularly among electronic financial support providers — which assist financial institutions with IT systems, data processing, security and authentication — and among “third-tier PG firms.” It defined third-tier PG firms as reseller or agency-type businesses that re-sell services based on contracts with second-tier PG firms.

A fintech industry official said that when businesses in the regulatory gray zone cause incidents, the fallout can spread across the entire industry. The official called for steps to improve transparency, including tightening rules to bring gray-zone operators into the system or blocking unqualified firms from entering the market.

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.