Caught between the two forces, South Korea's battery makers are pivoting aggressively toward energy storage systems and lower-cost chemistries to weather the global EV slowdown.

The clearest sign of Japan's retreat came on April 23, when Honda Motor announced it would end vehicle sales in South Korea by the end of 2026, closing out a 23-year presence in one of Asia's fiercest automotive battlegrounds.

Honda sold just 1,951 vehicles in Korea last year, down 85 percent from its 2008 peak of 12,356 units.

"It is regrettable to end business in Korea, but we will faithfully respond to consumers so they do not feel uneasy," said Lee Ji-hong.

Nissan Motor exited the Korean market in 2020, leaving only Toyota Motor and its luxury brand Lexus still selling passenger cars in the country.

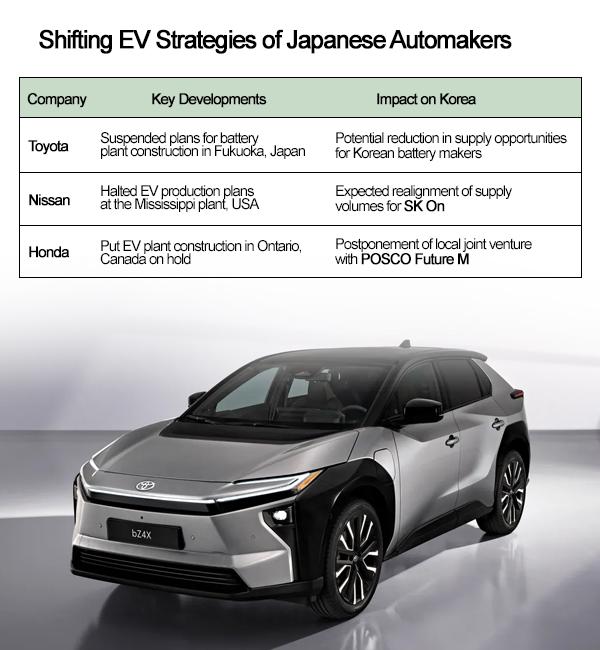

The pressure extends well beyond Korea.

The fallout is reverberating through Korea's battery industry.

SK on had agreed in March 2025 to supply 99 gigawatt-hours of high-nickel batteries for four next-generation Nissan EV models in a deal industry sources estimate at around 15 trillion won ($10.8 billion). The volume is now expected to be redirected to revised Nissan lineups, though final contract terms remain uncertain.

Honda's Ontario freeze has also forced Posco Future M to revisit a planned cathode joint venture in Canada, while the LG Energy Solution-Honda battery joint venture in Ohio is shifting output plans from pure EV batteries toward hybrid and energy-storage applications.

For Japan's automakers themselves, the outlook has darkened sharply.

Honda forecast a fiscal 2025 net loss of between 420 billion yen and 690 billion yen, potentially marking its first annual loss since listing publicly in 1957.

Nissan projects a 550 billion yen annual loss, while Toyota — still the world's largest automaker with 11.3 million vehicle sales in 2025 — faces an estimated $9.1 billion in U.S. tariff-related costs for the fiscal year ending March 2026.

As Japanese firms retrench, Chinese manufacturers are moving into the vacuum at unprecedented speed.

Chinese-built EVs, including Tesla vehicles exported from Shanghai, accounted for 33.9 percent of newly registered EVs in South Korea during the first quarter of 2026, up from just 4.7 percent in 2022, according to the Korea Automobile & Mobility Industry Association.

Domestic Korean brands' share fell to 57.2 percent from 75 percent over the same period.

BYD sold 5,991 vehicles in the first four months of 2026, ranking fourth among imported brands behind Tesla, BMW and Mercedes-Benz.

China's domestic EV market, however, is beginning to show signs of fatigue.

New-energy vehicle wholesale sales rose 28.2 percent in 2025 to 16.49 million units, accounting for nearly half of all vehicle sales in China. But BYD's monthly sales fell year-on-year for an eighth consecutive month in April as Beijing scaled back trade-in subsidies and prepared to reinstate purchase taxes.

The company compensated by accelerating exports, shipping a record 134,000 vehicles overseas in April alone, up 70.9 percent from a year earlier.

Beyond the China-Japan-Korea triangle, EV demand is broadening rapidly across emerging Asia.

India's electric passenger vehicle sales surged 87.4 percent in fiscal 2026 to 233,246 units, while total EV sales across two-, three-, four-wheelers and commercial vehicles reached 2.45 million units, according to Jato Dynamics.

Southeast Asia is moving even faster on EV penetration.

Battery-electric vehicles accounted for roughly 26 percent of new car sales in Vietnam through August 2025, driven overwhelmingly by local automaker VinFast and its VF 3 mini-SUV.

Thailand reported EV penetration of around 20 percent in the first 10 months of 2025, dominated by Chinese brands including BYD and Great Wall Motor. In Singapore, EVs already account for more than 40 percent of new car sales.

For Korea's battery trio — LG Energy Solution, Samsung SDI and SK on — the strategic response has been a rapid shift away from pure EV dependence.

All three are accelerating lithium iron phosphate battery production for grid-scale energy storage projects in North America, where changes to federal tax-credit policies have prompted automakers to slow EV investment and delay orders.

LG Energy Solution targets more than 60 gigawatt-hours of global ESS capacity this year, including over 50 gigawatt-hours in North America. SK On has already secured a 7.2 gigawatt-hour ESS supply agreement with Flatiron Energy Development.

"Demand for ESS is growing more sharply than ever before, and this is the crucial opportunity for the success of portfolio rebalancing," said Kim Dong-myung in his New Year address.

The pivot may offer Korean battery makers a bridge through the EV slowdown, but competition remains intense.

As Asia's automotive landscape fractures between retreating Japanese incumbents, surging Chinese exports and rapidly expanding emerging-market demand, Korea's battery industry — long viewed as the region's strongest electrification advantage — is entering its most consequential test yet.

Copyright ⓒ Aju Press All rights reserved.