SEOUL, May 19 (AJP) - South Korea’s household debt climbed to the brink of the symbolic 2,000 trillion won ($1.33 trillion) threshold as of March as tighter bank regulations failed to stop a fresh wave of housing-related borrowing that increasingly migrated to non-bank lenders.

Outstanding household credit reached 1,993.1 trillion won at the end of March, up 14 trillion won, or 0.7 percent, from the previous quarter, according to preliminary data released by the Bank of Korea (BOK) on Tuesday.

The annual growth rate accelerated to 3.5 percent from 2.9 percent in the fourth quarter.

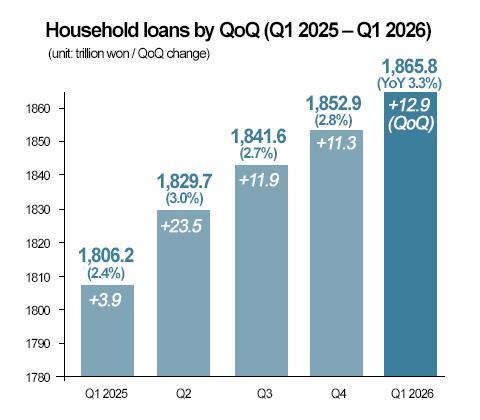

Household loans accounted for 1,865.8 trillion won of the total, rising 12.9 trillion won on quarter, while credit card and installment debt increased 1.1 trillion won to 127.3 trillion won.

The increase was driven overwhelmingly by housing demand rather than consumer spending, underscoring how Korea’s property market continues to fuel leverage despite prolonged efforts by regulators to cool borrowing.

Housing-related loans — a newly renamed category previously classified as mortgage loans — expanded by 8.1 trillion won in the January-March period, up from a 7.2 trillion won increase in the previous quarter.

Other loans, including personal credit lending, also rose at a faster pace, increasing 4.8 trillion won after a 4.1 trillion won gain three months earlier.

The more striking shift came from where the borrowing occurred.

Commercial bank household lending, which had increased by 6 trillion won in the fourth quarter, swung to a 200 billion won decline in the first quarter as tighter lending controls curbed bank-based mortgages. But the slowdown merely pushed borrowers toward secondary lenders.

Loans extended by non-bank depository institutions nearly doubled in growth pace to 8.2 trillion won from 4.1 trillion won in the previous quarter, according to the BOK. Housing-related lending at those institutions surged 10.6 trillion won, sharply accelerating from a 6.5 trillion won increase three months earlier.

Mutual finance cooperatives accounted for 5.1 trillion won of the increase, while Saemaul Geumgo, or MG Community Credit Cooperatives, added another 2.4 trillion won.

“The recent rise in housing transactions means we need to closely monitor related lending trends,” Lee Hye-young, head of the Financial Statistics Team at the BOK, said during a briefing.

The data suggest regulators may be containing risk within the banking sector only to see leverage resurface elsewhere in the financial system — a recurring concern in Korea’s long-running household debt cycle.

By contrast, signs of consumer weakness remained limited. Growth in merchandise credit slowed to 1.1 trillion won from 3 trillion won in the previous quarter, but the central bank said seasonal factors likely accounted for much of the moderation, noting that card spending typically peaks in year-end quarters.

In a notable methodological change, the BOK also began separately disclosing jeonse loans — financing tied to Korea’s lump-sum rental deposit system — from commercial banks. The central bank said the split was necessary because such loans have expanded rapidly over the past decade and have become increasingly important in assessing housing-related debt risks.

Outstanding jeonse loans at commercial banks reached 165.7 trillion won at the end of March, accounting for 16.6 percent of total commercial bank household lending. The figure has surged more than sixfold since 2015, when related balances stood at just 25.3 trillion won.

Copyright ⓒ Aju Press All rights reserved.