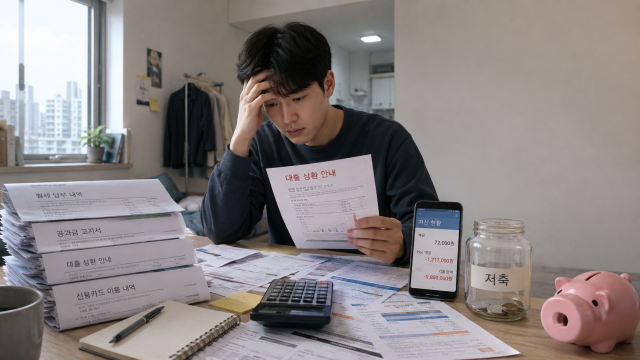

The government has introduced various asset formation policies for young people, including the Youth Future Savings program. However, the financial reality for many young adults is more about managing debt than saving. Young people have recorded the highest loan delinquency rates among all age groups, with many resorting to borrowing to cover living expenses. This raises concerns that, contrary to the government's focus on savings, debt management has become a more pressing issue for a significant number of young adults.

As of the end of March this year, the average delinquency rate for household loans among those under 20 at the five major banks—KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup—was 0.44%, the highest across all age groups. Those aged 60 and above followed closely with a rate of 0.41%, while the rates for those in their 50s and 40s were 0.36% and 0.32%, respectively. The lowest rate was 0.22% for those in their 30s.

Although the delinquent balance for those under 20 was 125.3 billion won, the smallest among all age groups, the high delinquency rate suggests that young adults are relatively more vulnerable in terms of repayment capacity.

Financial experts note that young adults often have limited income and insufficient financial assets, making them more susceptible to delinquency when faced with short-term expenses like living and housing costs.

The primary factor reducing the savings capacity of young adults is the burden of living expenses. A survey conducted by the Seoul Financial Welfare Counseling Center last year found that 67.9% of 1,025 young individuals under 29 who applied for personal rehabilitation cited covering living expenses as the main reason for incurring debt. Many are turning to credit cards or loans to fill the gap, indicating a growing trend of prioritizing debt repayment over savings.

Given this situation, it remains to be seen how effective asset formation policies targeting young adults will be in reaching those most in need. The Youth Future Savings program, which is open for enrollment this month, aims to support long-term savings for young people but requires a certain income level and monthly contribution capacity. For those currently lacking income or struggling with living expenses and debt repayments, both enrolling in and maintaining the program may prove challenging.

Similar limitations have been observed with the existing Youth Leap Account. Participants in this program have an average credit score of 876.2, higher than the overall average of 814.1 for young people. This suggests that those with better financial conditions and higher credit scores are benefiting more from these policies, potentially leaving the most vulnerable young adults further distanced from institutional support.

The government is aware of the challenges faced by vulnerable young adults who are often excluded from existing policy frameworks. Recently, the Office of National Integration at the Presidential Office held discussions with young people in caregiving roles, those experiencing isolation, and youth preparing for independence to address the difficulties faced by those in policy blind spots. However, current financial policies for young people are primarily designed to support asset formation, which may not adequately address the needs of those already burdened by debt.

A financial sector representative stated, "While youth asset formation policies are necessary, many young people are more concerned about managing living expenses and debt repayments than saving. An approach that addresses both savings support and debt management is essential."

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.