This time, however, the story is fundamentally different.

From South Korea’s won and Indonesia’s rupiah to the Philippine peso, parts of Asia have come under renewed pressure as Gulf energy disruptions raise inflation risks, U.S. interest rates remain elevated and Asian savings increasingly migrate toward dollar assets.

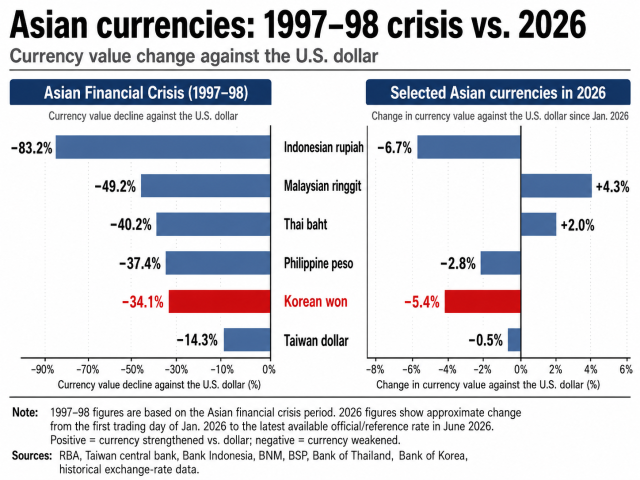

The pressure is not uniform. The Indonesian rupiah has weakened more sharply than the won this year, while the Philippine peso has also struggled. The Malaysian ringgit and Thai baht have been more resilient on a year-to-date basis, but remain exposed to the same forces: energy costs, dollar rates and shifting capital flows.

Yet policymakers are showing little of the panic that once accompanied such numbers. This time, the pressure is less about Asia running out of dollars than about Asian savings moving into dollar assets.

That distinction may define a new era of currency management across the region.

The average value of the won against the U.S. dollar in June has slipped to its weakest level since 1998, when South Korea was under an International Monetary Fund bailout.

According to Bank of Korea data, the won traded at an average of 1,521.4 per dollar between June 1 and 19, based on daytime closing prices in Seoul.

The average marked the weakest monthly level since February 1998, when the won averaged 1,626.7 per dollar. It was also weaker than the 1,453.3 average recorded in March 2009 during the global financial crisis. The won has remained above the psychologically important 1,500 level for 24 consecutive trading sessions since May 15.

Yet the resemblance to earlier crises largely ends there.

Asia’s currency pressure is broad, but uneven

The Indonesian rupiah, Malaysian ringgit and Thai baht have all experienced even larger declines this year, while Taiwan and India have seen substantial foreign capital outflows.

Taiwan has recorded roughly $22 billion in equity outflows and India about $31 billion. South Korea has experienced an even larger withdrawal, with around $78 billion leaving the market by June 12.

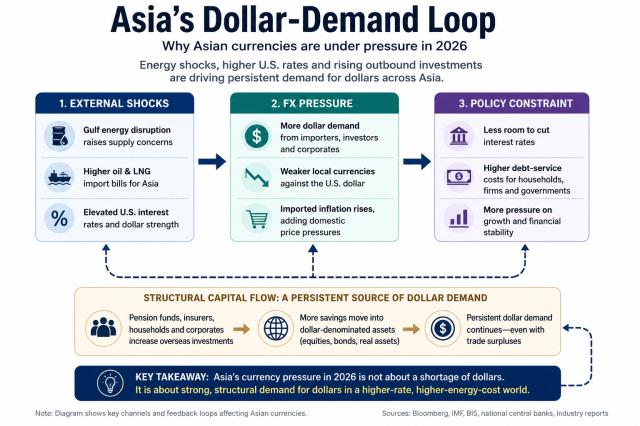

Several forces are converging simultaneously.

The Gulf conflict has revived concerns over energy security. The Federal Reserve has maintained a higher-for-longer interest rate stance. At the same time, Asian investors themselves are increasingly allocating savings and leveraged funds to U.S. equities and other dollar-denominated assets.

The result is a region-wide imbalance in which structural demand for dollars is steadily overwhelming traditional support from trade surpluses.

That is a very different phenomenon from the one that destabilized Asia nearly three decades ago.

The latest Gulf tensions have reminded policymakers that Asia remains uniquely exposed to energy disruptions.

About a fifth of global oil and liquefied natural gas trade passes through the Strait of Hormuz, and many Asian economies remain heavily dependent on Middle Eastern supplies.

South Korea imports more than 70 percent of its crude oil from the region. Japan, Taiwan and India also rely heavily on Gulf energy.

Every spike in oil prices now carries a triple effect.

Higher import bills weaken currencies. Weaker currencies amplify imported inflation. Inflation risks, in turn, limit central banks' ability to cut interest rates to support growth.

The dynamic has become particularly challenging because it is colliding with another long-term trend: Asia's capital is increasingly moving abroad.

In late 1997, South Korea's official foreign exchange reserves stood at just $24.2 billion, while usable reserves had fallen to only $9.2 billion. More than half of the country's $120 billion in external debt was short-term borrowing due within a year.

Today, the numbers tell a different story.

South Korea held $426.99 billion in foreign exchange reserves at the end of May. It posted a $28.29 billion current account surplus in April, while its net international investment position stood at $753.6 billion at the end of the first quarter.

These are hardly the balance sheets of an economy facing a solvency crisis.

The stress is instead emerging from the financial account.

In other words, Korea is not suffering from a shortage of dollars. It is facing an abundance of won chasing dollars.

The same pattern is increasingly visible elsewhere in Asia.

Korea's vulnerability stems from several overlapping factors.

The interest rate gap with the United States remains significant. The Bank of Korea's benchmark rate stands at 2.5 percent, while the upper bound of the Federal Reserve's target range remains at 3.75 percent.

The differential makes dollar assets more attractive than won-denominated investments.

At the same time, foreign investors have become persistent sellers of Korean equities.

According to the Bank of Korea, foreign investors withdrew a net $31.83 billion from Korean stocks in May, the largest monthly outflow since comparable data began.

Bond inflows of $5.68 billion were nowhere near enough to offset the exodus.

Paradoxically, Korea's stock market rally has amplified the pressure.

The KOSPI continues to set record highs, expanding the value of foreign-held shares. Even modest profit-taking can therefore generate substantial dollar demand.

Asia's capital is becoming a global market force

The growing importance of East Asian capital has become significant enough to draw attention from Washington.

U.S. Treasury Secretary Scott Bessent has repeatedly underscored the importance of Asian currencies, capital flows and monetary policy decisions as factors that can influence global financial markets.

Japan's decision to raise interest rates to 1 percent for the first time in more than three decades has exposed a new source of anxiety in Washington: the possibility that Asian capital could flow back home.

Japanese households and institutions collectively hold some of the world's largest pools of overseas assets, including roughly $1.1 trillion in U.S. Treasuries, making Japan the largest foreign holder of American government debt.

According to Japanese media reports, Bessent privately encouraged Japanese policymakers to normalize monetary policy sooner rather than later, warning that delaying action could eventually require more aggressive tightening.

The episode highlights an increasingly important reality.

Asian interest rates no longer matter only for domestic economies. They have become global financial variables.

Higher Japanese yields could encourage domestic investors to repatriate funds, reducing demand for U.S. Treasuries and potentially pushing up borrowing costs in the United States itself.

Domestic liquidity is adding another layer of pressure.

Broad money, or M2, rose 5.7 percent year-on-year in April, reaching 4,153.9 trillion won.

At the same time, Korean households, pension funds and institutions continue accelerating their overseas investments.

The National Pension Service plans to raise its allocation to overseas equities to 37.2 percent by the end of this year, up from 35.9 percent.

Institutional investors already held more than $500 billion in foreign securities at the end of March.

The trend reflects a broader shift in investor behavior.

South Korea is no longer merely an export-driven economy. It is becoming a major exporter of capital.

That creates recurring dollar demand, leaving the won more vulnerable whenever global rates, energy prices or foreign equity flows turn against Korea.

Copyright ⓒ Aju Press All rights reserved.