[Source: Bank of Korea]

The amount of non-performing loans (NPLs) at domestic banks has surged from 9.7 trillion won to 17.7 trillion won over the past three and a half years, primarily affecting small businesses and individual entrepreneurs rather than large corporations.

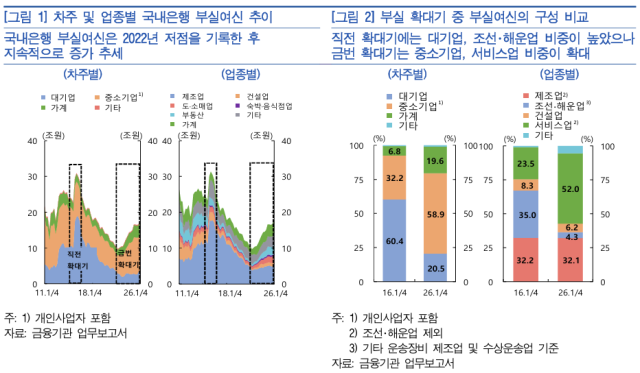

According to the Financial Stability Report released by the Bank of Korea on June 24, the total non-performing loans at domestic banks reached 17.7 trillion won as of March 2026, up from a low of 9.7 trillion won in September 2022.

This increase in non-performing loans marks a departure from previous trends. During the last significant rise in NPLs from 2015 to 2016, the shipping and shipbuilding industries were primarily responsible, with large corporations accounting for 60.4% of non-performing loans in the first quarter of 2016.

In contrast, since 2022, the current increase has been driven by small businesses. As of the first quarter of this year, small businesses represented 58.9% of non-performing loans. The slow recovery in domestic service sectors, such as retail and real estate, has led to a broader spread of financial distress across various industries.

The scale of loan restructuring has also expanded, focusing on small businesses. Last year, the amount of loan restructuring for small businesses reached 14.8 trillion won, accounting for 66.4% of the total restructuring amount of 22.3 trillion won.

Notably, there has been a significant increase in the sale of non-performing loans. Last year, the volume of NPL sales reached 8.2 trillion won, making up 36.7% of the total restructuring amount. In comparison, write-offs were 6 trillion won (27.1%), and loan recoveries were 4.5 trillion won (20.4%).

The Bank of Korea analyzed that banks find it more advantageous to manage non-performing loans through sales rather than through self-recovery or debt restructuring. The increased participation of specialized NPL investment firms has also contributed to the rise in sales.

The nature of the non-performing loans being sold has changed as well. In 2015, corporate borrowers accounted for 77.2% of non-performing loan sales due to the restructuring in the shipping and shipbuilding sectors. However, last year, the share of individual borrowers, including small business owners, rose to 41.5%, nearly doubling from 22.8% in 2015.

The types of collateral have also shifted. In 2015, industrial assets made up 59.1% of collateral, but this figure dropped to 40.3% last year. Conversely, the share of commercial property collateral increased from 20.5% to 31.7%, while residential property collateral rose from 11.7% to 20.1%.

The Bank of Korea acknowledged that proactive management of non-performing loans is contributing to improvements in asset quality, but it also expressed caution regarding potential future risks.

The Bank stated, "If market interest rates rise while economic conditions remain poor or the recovery of borrowers' repayment abilities is delayed, the likelihood of further increases in non-performing loans is high. The banking sector needs to closely monitor market supply and demand when selling NPLs and diversify its approaches to managing non-performing loans while focusing on proactive risk management."

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.