The Bank of Korea assessed on June 24 that the country’s financial system is generally stable, although it noted potential risks stemming from increased volatility in financial and foreign exchange markets and concerns over the deterioration of vulnerable sectors.

According to the financial stability report released by the Bank of Korea, the financial instability index, which comprehensively reflects the short-term stability of the financial system, recorded a cautionary level of 17.2 in May this year. The financial vulnerability index, indicating medium- to long-term weaknesses, stood at 46.0 in the first quarter of this year, slightly above the long-term average of 45.7 since 2008.

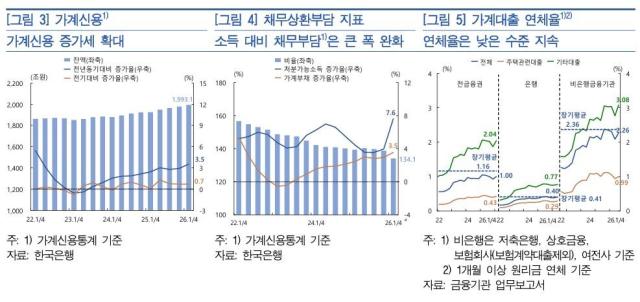

The Bank explained that both household and corporate credit expanded in the first half of this year. Household loans increased significantly due to rising demand for home purchases and stock-related loans, while corporate loans also saw a slight uptick, primarily driven by lending to banks and large corporations. The delinquency rate for household loans remained below the long-term average, but the delinquency rate for corporate loans has risen this year, exceeding the long-term average.

Lee Jae-joon, Deputy Governor of the Bank of Korea, stated, "Thanks to the growth in nominal GDP, the household debt ratio is declining faster than expected, which has somewhat alleviated overall risk. However, it remains at a relatively high level compared to major countries, and qualitative vulnerabilities such as the debt service ratio (DSR) persist. Given the recent expectations of rising real estate prices, it is necessary to manage household loans with caution."

In the external sector, the foreign exchange market has experienced high volatility due to factors such as the situation in the Middle East and the flow of domestic and foreign investment funds, although the conditions for foreign currency procurement have remained favorable. This year, foreign investment in domestic securities has shown a net outflow, particularly in stocks, while overseas investment by residents has slowed. The country’s external payment capacity remains robust, despite a slight decline in external soundness indicators.

Deputy Governor Lee noted, "The depreciation of the won against major advanced currencies was largely due to profit-taking and rebalancing rather than the fundamentals of our economy. Considering the recent current account surplus, we expect the exchange rate to stabilize gradually. We are monitoring the situation closely and are prepared to take measures to ensure market stability if high exchange rates, which deviate from fundamentals, persist or volatility increases excessively."

The Bank of Korea has maintained the base rate at 2.50% since the second half of last year but indicated that it may need to raise rates at an appropriate time, considering inflationary pressures, economic trends, and financial stability risks.

Concerns about the deterioration of vulnerable sectors due to rising interest rates were highlighted. The Bank noted that while rising market interest rates could have a positive effect by alleviating financial imbalances, they could also lead to increased volatility in financial markets and the potential for prolonged deterioration in vulnerable sectors.

Furthermore, if profit-taking funds from the stock market flow into the housing market, the positive effects of rising loan rates on financial imbalances could be diminished. Therefore, it is essential to manage expectations of rising housing prices consistently to prevent excessive capital inflow into the housing market.

In the real estate market, housing prices have rebounded in the Seoul metropolitan area. The asset soundness of financial institutions showed varying trends by sector, but overall profitability has improved.

Hwang Geon-il, a member of the Financial Monetary Committee overseeing the financial stability report, expressed concerns about rising household debt. He stated, "The ongoing increase in housing prices, particularly in the metropolitan area, and the rise in leveraged asset investments have raised concerns about household debt once again. We need to be mindful of the potential risks to financial stability stemming from deepening polarization across various sectors of the economy."

Hwang emphasized the need for proactive efforts to address polarization and structural improvements, in addition to supporting vulnerable sectors in a timely manner. He stated, "For real estate project financing (PF), which has seen significant deterioration, we should pursue continuous restructuring for a soft landing. For self-employed individuals, who represent a significant portion of our economy, we need a comprehensive response that combines financial support and debt restructuring based on repayment capacity, along with coordinated policies across finance, industry, employment, and welfare at each stage of business development."

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.