SEOUL, March 03 (AJP) — Is the two-year bull run in Seoul finally running out of steam, or will the market once again absorb an oil shock and move on?

Tuesday’s verdict was brutal. The KOSPI plunged 7.24 percent to 5,791.91, while the tech-heavy KOSDAQ fell 4.62 percent to 1,137.70 — one of the sharpest single-day routs in recent memory.

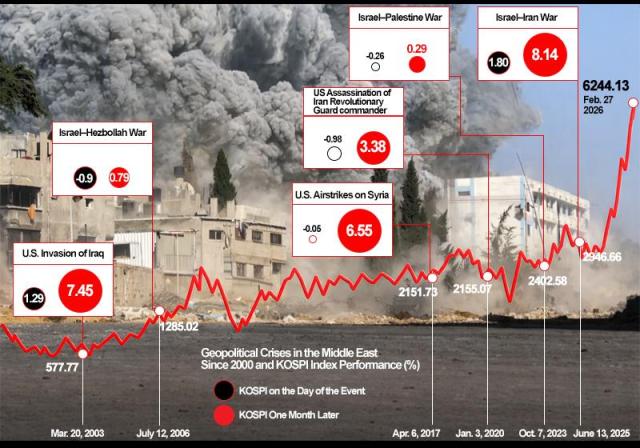

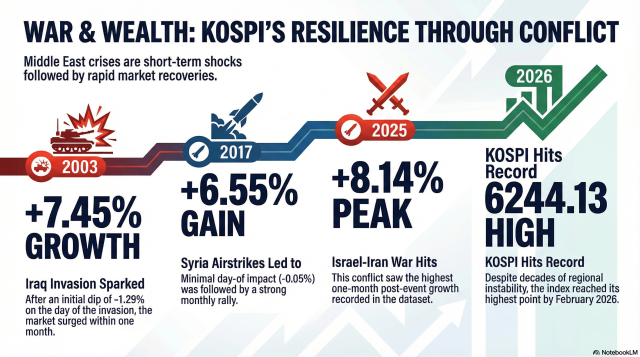

History offers some comfort. In six major Middle East military crises since 2000, the KOSPI was positive one month after each event. The initial reaction varied — often violent — but the pattern was consistent: unless energy supply was materially disrupted, the shock faded.

This time, however, investors are not entirely convinced.

Hur Joon-young, professor of economics at Sogang University, warned that markets may be underestimating the political dynamics inside Iran.

“In previous confrontations, tensions rose but stopped short of prolonged direct war,” Hur said. “If internal pressures within Iran intensify, the conflict could extend beyond the two- to four-week window currently assumed.”

He also noted a recurring military lesson: air power alone rarely delivers decisive outcomes. If limited strikes evolve into broader engagement, uncertainty — particularly around energy flows — could persist longer than markets expect.

Political calculations in Washington and Jerusalem add another layer of unpredictability. Domestic pressures on leadership could increase escalation risk rather than contain it.

In short: the question is not whether there is conflict, but how long it lasts.

Markets do not price war; they price oil.

The U.S. Energy Information Administration estimates roughly 20.9 million barrels per day transit the Strait of Hormuz — about one-fifth of global petroleum liquids consumption and nearly one-third of seaborne oil trade.

History reinforces the point. During the 1990–1991 Gulf War, Brent crude surged toward $40 before easing as supply fears receded. The market reaction depended less on combat itself and more on the durability of supply disruption.

If Hormuz flows remain intact, volatility may prove temporary. If they do not, inflation expectations could quickly reprice.

The equity response is already bifurcated.

Refiners and energy names have rallied on margin expectations. Over the past three months, S-Oil has surged 41.57 percent and SK Innovation 9.71 percent.

Defense stocks are in full repricing mode. Hanwha Aerospace jumped nearly 20 percent Tuesday alone, with LIG Nex1 and Hanwha Systems up roughly 30 percent. Brokers cite potential replenishment demand for missile systems in the Gulf, including the Cheongung interceptor and Chunmoo rocket platform.

The structural defense bid predates this crisis. Over three months, Hanwha Systems is up 145 percent, Korea Aerospace Industries 75 percent, and Hanwha Aerospace 38 percent.

Airlines and travel stocks, by contrast, now face the familiar double hit of fuel costs and demand risk.

This is not indiscriminate panic. It is rotation.

The counterargument to the selloff is simple: earnings momentum remains intact.

Daishin Securities recently lifted its year-end KOSPI target to 7,500 from 5,800, applying forward EPS of 728 and a 12-month PER of 10.32 — broadly in line with post-2021 averages.

Forward EPS estimates have already climbed from 555 at end-January to around 610, a 10 percent upward revision. Further sector upgrades could add nearly 14 percent to profits, with semiconductors accounting for the bulk.

Kiwoom Securities notes the KOSPI trades just above 10 times forward earnings, with February exports up 29 percent year-on-year, led by chips.

If earnings continue to rise, geopolitics may prove noise rather than regime change.

The real macro risk lies in second-round effects.

If oil prices stay elevated long enough to reignite inflation, expectations for global rate cuts will recede. That would pressure valuation multiples just as earnings optimism peaks.

Bond markets are already flashing caution.

Short-term yields have risen faster than long-term rates, reflecting inflation sensitivity and diminishing expectations for Bank of Korea easing. A sustained move higher in U.S. Treasury yields would tighten global liquidity — the one variable equities struggle to ignore.

Kiwoom’s base case assumes stabilization within a week, even with partial oil disruptions. But sensitivity rises sharply if Hormuz flows are impaired for any sustained period.

Markets have historically absorbed geopolitical crises. The S&P 500, for instance, often fell on the first day of Middle East conflicts but recovered within weeks if energy supply remained stable.

Copyright ⓒ Aju Press All rights reserved.