The Yoon Suk Yeol administration has signaled a clear intention to stimulate the stock market since taking office. For the market to thrive, liquidity and transactions are essential. Revisions to commercial law, the elimination of the financial transaction tax, and expectations surrounding retirement pensions have led to an influx of liquidity into the stock market, opening the door for trading.

In stark contrast, the government has indicated a desire to end the era of profiting from real estate, simultaneously reducing both fuel and oxygen to prevent further market overheating. Unlike past strategies that relied solely on taxation, the current approach tightens liquidity through lending restrictions and curtails transactions with increased capital gains taxes and land transaction permits.

The plan to position stocks as an alternative asset to real estate has seen some success. Speculative transactions in Gangnam have noticeably decreased, leading to an increase in urgent sales and a temporary drop in home prices. Notably, the shift in strategy to rely on finance and supply rather than just taxes is commendable. In stock market terms, this has effectively halted the short-term surges of overheated stocks, resulting in divergent trends between the two markets.

KOSPI Hits 8000, Gangnam Faces Trading Cliff

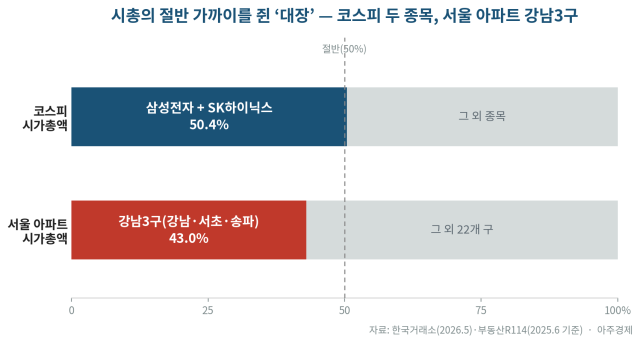

While the KOSPI is led by major stocks like Samsung Electronics and SK Hynix, the real estate market's equivalent is the Gangnam area. Over the past year, while the stock market leaders surged with trading volume, the Gangnam area moved in the opposite direction. Lending restrictions have limited buyers' access to funds, increased capital gains taxes have reduced sellers' incentives, and land transaction permits have restricted investment demand. The number of apartments for sale in Seoul has decreased by about 25% compared to a year ago, with urgent sales in Gangnam being absorbed first, leading to a stabilization of asking prices.

In stock market terms, Gangnam is not a halted stock but rather a major stock with dwindling supply. Sellers are constrained by taxes, while buyers are hindered by lending restrictions and land transaction permits, resulting in thin transaction volumes. In a market with limited supply, prices are less likely to drop even with fewer transactions. This is why Gangnam began to recover after urgent sales were absorbed in May, just before the end of the grace period. However, the lack of sufficient transaction volume makes it difficult to confirm this rebound as a trend reversal.

Average price increases in Seoul do not fully capture the market's true condition. Rather than collapsing under pressure or flooding the market with urgent sales, some homeowners have opted to withdraw their listings to hold firm. With the end of the grace period for increased capital gains taxes approaching, urgent sales were absorbed first, and after the end of the grace period, the supply of listings decreased, leading to a resurgence in asking prices.

Ultimately, the three districts of Gangnam resemble high-quality stocks that have not easily succumbed to demand despite repeated regulations. The current trading drought is more akin to a correction phase due to external factors than a fundamental deterioration. While transaction volumes in Gangnam have dried up, market demand has not vanished.

Real Estate Demand Persists Despite Market Challenges

This is where real estate diverges from stocks. In the stock market, reduced liquidity and trading quickly cool off overheating. However, in real estate, there remains a genuine demand to buy. The liquidity that has dried up in Gangnam has circulated to areas outside of regulations. As trading restrictions were imposed on the major stock of Gangnam, the money did not disappear; it returned to stocks outside of regulations.

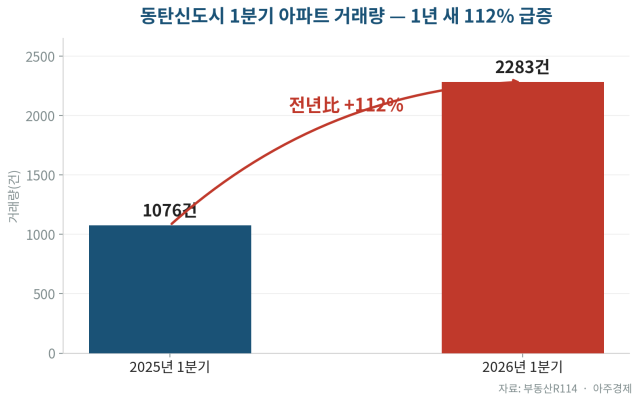

The first area to attract this circulating demand is Dongtan in Hwaseong. Not classified as a regulated area under the 10-15 measures, it has relatively loose requirements for actual residence and fewer restrictions on taxes and loans, leading to a 112% surge in apartment transactions in Dongtan New Town in the first quarter compared to a year ago. However, it cannot be viewed solely as a speculative theme stock. The area has fundamental support due to its proximity to the semiconductor belt, expectations surrounding the opening of the GTX-A line, and a 1.5% internal loan liquidity. Reports indicate that the demand from employees of semiconductor companies like Samsung Electronics and SK Hynix, along with the availability of internal loans, has bolstered the buying momentum in Dongtan.

Not all demand that was stifled in Gangnam has shifted to non-regulated areas like Dongtan. Some buyers have postponed purchases and remained in the Seoul rental market. While the demand for buying has lingered in the rental market, the actual residence requirements and the conversion of rental properties into sales have led to a decrease in rental listings. The average rent for apartments in Seoul rose by 0.28% in the second week of May, marking the highest increase in nearly 10 years since November 2015, while rental listings decreased by 23.5% over three months.

Focus on Supply and Transactions, Not Prices

So what should be the focus? The trading drought observed earlier reflects the current market's strength, while supply indicates the strength of the next cycle. Just as stock investors look at trading volume and supply rather than indices, real estate should also focus on transactions and supply rather than prices. However, supply is dwindling. This year, the number of apartments ready for occupancy in Seoul is expected to be around 20,000, half of previous years, and housing permits in the first quarter plummeted from 14,966 units to 5,632 units, a 62% decrease year-over-year.

Permits are a leading indicator showing supply capacity three to five years down the line, not immediate occupancy. The combination of this year's shortage of new units and a sharp decline in permits suggests a growing rental crisis now and a future supply gap. The direction to resolve this through supply is correct, but the challenge lies in the speed. While the government has promised 1.35 million units in the metropolitan area by 2030, it will take time for the market to feel the impact of this supply.

Not all liquidity has spread evenly. Just as major growth stocks and neglected stocks diverge, core areas, industrial belts, and rural outskirts are following different trajectories. The nationwide housing quintile ratio reached a record high of 12.8 times at the end of last year. Additionally, there are still concerns regarding interest rates. While interest rates serve as a discount rate in stocks, they represent monthly repayment amounts in real estate. If regulations are lifted or interest and loan conditions change in a supply-constrained environment, pent-up buying demand could push prices higher again.

Real Estate Must Be Viewed Through Its Own Lens

Real estate is not the same as stocks. A decrease in transactions does not equate to a disappearance of demand, nor does a drop in prices mean a reduction in housing cost burdens. When purchases are restricted, some buyers move to non-regulated areas, while others remain in the rental market. If rentals become constrained, the market shifts to monthly leases. Supply does not increase immediately upon placing orders; there are years of lag between permits, construction, completion, and occupancy. While stock investors focus on liquidity and trading volume, real estate investors must consider the people and time that remain behind.

The government has had some success in curbing speculative trading in Gangnam. However, the trend of price stabilization has not lasted long. Gangnam has managed to hold its asking prices and rebound, while some demand has shifted to Dongtan, and some has remained in the rental market, pushing up housing costs. The government has not fully anticipated when and how the next supply gap will impact the burden on residents. Real estate policy should not end with suppressing the market to buy time. If time has been bought with a stock investor's perspective, then housing must be built for people to live in during that time, as real estate ultimately concerns where people reside.

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.