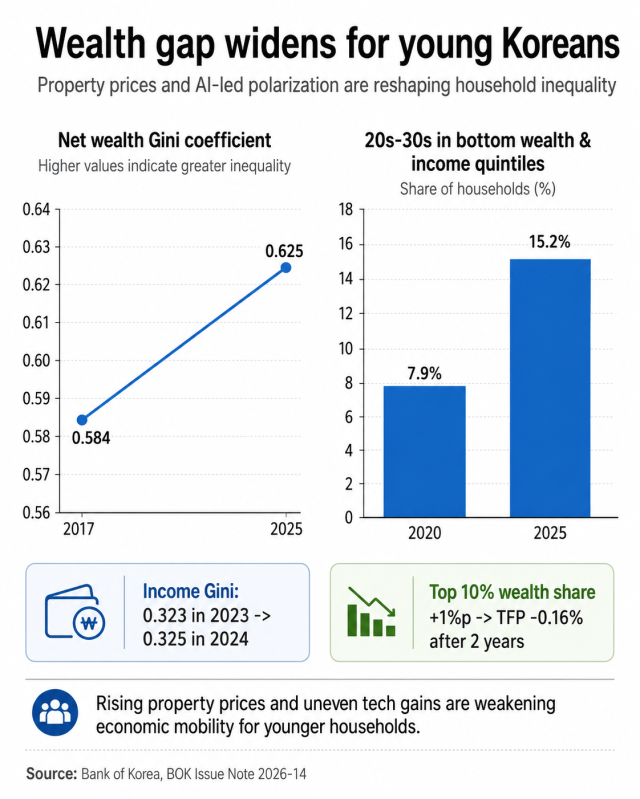

Rising real estate prices have widened wealth gaps between homeowners and non-homeowners, regions and generations. The net wealth Gini coefficient rose to 0.625 in 2025 from 0.584 in 2017, with a higher reading indicating a more unequal distribution.

The central bank identified rising property prices as the main driver of the widening wealth gap. Property ownership is concentrated among older households, making intergenerational wealth inequality more entrenched.

The trend has weakened the wealth-building ladder for young people. A growing number of high-income young Koreans are unable to move into the upper wealth bracket because they do not own property, a phenomenon similar to the so-called HENRY group, or "High Earners, Not Rich Yet."

K-shaped growth, marked by strong IT manufacturing and sluggish growth in non-IT sectors, has widened wage gaps across industries. Artificial intelligence could add further pressure by replacing tasks performed by low-income workers and young people at the early stages of their careers.

A BOK survey showed that lower-income groups were more likely to believe their jobs could be replaced by AI, while their actual use of AI was lower than that of higher-income groups.

Employment data also showed signs of pressure on young people. Youth employment has fallen faster in industries with high exposure to AI since the launch of generative AI, while employment among people in their 50s has increased in those sectors.

The BOK described the trend as "seniority-biased technical change."

The combined wealth and income divide is lowering the economic standing of young households. The share of households in both the bottom net wealth and income quintiles that were headed by people in their 20s and 30s rose to 15.2 percent in 2025 from 7.9 percent in 2020.

Household polarization could hurt productivity and domestic demand. A panel analysis of 120 countries cited by the BOK showed that a 1 percentage point rise in the wealth share of the top 10 percent lowers total factor productivity by 0.16 percent two years later.

The concentration of household assets in real estate can reduce the efficiency of resource allocation by keeping capital tied up in unproductive assets rather than innovative companies and new technologies.

Higher housing costs could also reduce discretionary spending by young and low-income households, which tend to have a higher propensity to consume. Broader social costs could increase if people believe wealth gaps cannot be overcome through work alone.

High housing costs could also weigh on marriage and childbirth among young people.

The BOK said traditional income-support policies are not enough to address the problem. It called for policies that encourage household assets to move away from real estate and into more productive sectors, while expanding wealth-building channels for young and non-homeowning households.

The central bank also urged policymakers to redesign redistribution systems for the AI era, strengthen job training for workers exposed to technological displacement and broaden the tax base as labor income becomes more vulnerable to automation.

Copyright ⓒ Aju Press All rights reserved.