The education tax burden on securities firms has reached alarming levels. Following last year's tax reform that raised the education tax rate, the booming domestic stock market and rapid growth of the exchange-traded fund (ETF) market have led to a more than threefold increase in education tax burdens compared to the previous year. Critics point out that the newly established highest tax rate for education tax, combined with the current law's disregard for netting gains and losses on securities, has resulted in tax burdens exceeding actual net profits for securities firms.

According to the financial investment industry on June 18, the estimated education tax payments for four major domestic securities firms—Kiwoom, NH, Meritz, and Shinhan—totaled approximately 68.4 billion won in the first quarter of this year. This marks a 3.48-fold increase from the 19.6 billion won reported during the same period last year. Notably, considering that these firms collectively paid about 103.8 billion won in total education tax last year, they have already accounted for 66% of last year's total tax amount in just three months.

Other securities firms are also expected to see significant increases in their education tax burdens compared to last year. The industry anticipates that the total education tax for this year will rise several times over from the previous year.

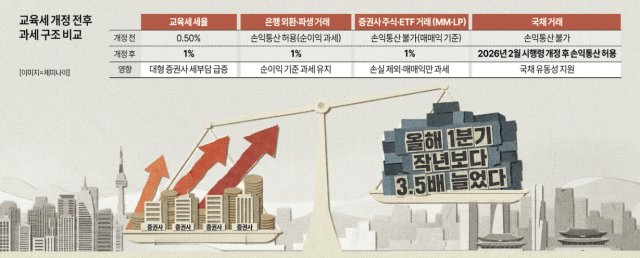

The surge in education tax burdens is attributed to the increase in the education tax rate from 0.5% to 1% for large financial and insurance companies with annual excess earnings exceeding 1 trillion won, effective this year. The booming stock market has also significantly expanded the taxable base for securities firms.

The rise in the domestic stock market and increased volatility have greatly expanded the trading volume for market makers (MM) and liquidity providers (LP) in the ETF sector. According to the Capital Market Research Institute, the trading profits of the top 10 securities firms based on equity capital are projected to surge from 7.2 trillion won in 2024 to 49.5 trillion won this year, nearly a sevenfold increase. The proportion of trading profits in total net income is also expected to rise from an average of 130% in the past to 364% this year.

However, the current education tax law stipulates that the taxable base for trading profits does not reflect the actual net income earned by securities firms. While banks calculate education tax based on net income from foreign exchange and derivatives trading, securities firms are taxed solely on trading profits without accounting for losses incurred in individual transactions.

In the process of providing liquidity to stabilize prices for market making and ETFs, securities firms must engage in hedging transactions by buying and selling underlying stocks to mitigate price volatility risks. Even if the final net profit from these transactions is minimal, tax authorities impose taxes based on the total trading profits, excluding losses. As a result, the gap between actual net profits and the taxable base for education tax widens as market volatility increases. This creates situations where firms must pay education tax even when they report net losses.

In February, the government amended the enforcement decree of the education tax law to allow netting of gains and losses only for government bonds. However, stocks and ETFs were excluded from this provision. With the domestic stock-type ETF net assets surging from 35 trillion won at the end of 2024 to 260 trillion won as of yesterday, the tax burden has disproportionately increased for larger firms.

A representative from a major securities firm stated, "The education tax is initially calculated based on estimated amounts monthly and quarterly, and the final taxable base is confirmed at year-end. Typically, as the year progresses, the taxable base tends to increase rather than decrease, so considering the cumulative effect in the second half of the year, the final total tax amount could exceed expectations."

He added, "While the government is promoting policies to invigorate the stock market, it is imposing a burdensome and distorted tax structure on liquidity providers that support market infrastructure. If the tax burden continues, securities firms will have no choice but to reduce their market-making and LP contracts, ultimately leading to decreased market liquidity and weakened price discovery, which will adversely affect retail investors."

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.