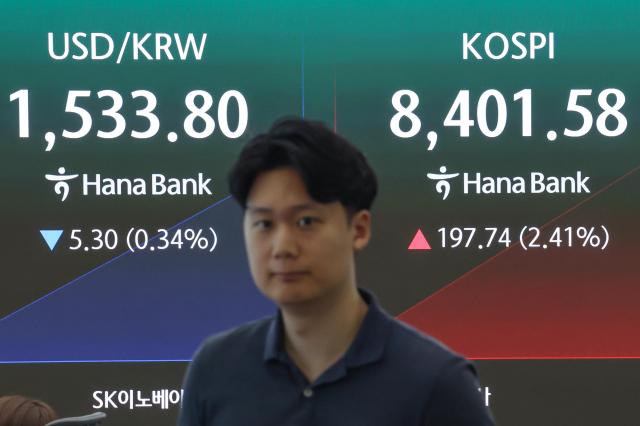

SEOUL, June 24 (AJP) - The stock market rebounded, but the Korean won slipped deeper toward crisis-era lows after South Korea once again failed to make MSCI's developed-market watchlist, a sober reminder that the currency - not the equities - is the stumbling block to an upgrade.

The KOSPI has quadrupled over the past 18 months to become one of the world's best-performing equity markets since 2025, but its rally alone was not enough.

For years, Seoul has tried to secure MSCI developed-market status by improving market accessibility through English-language disclosures, settlement systems and extended foreign-exchange trading hours.

Fellow index provider FTSE Russell has classified South Korea as a developed market since 2009, but MSCI remains unconvinced.

In its annual review Tuesday, MSCI acknowledged the progress but pointed to a familiar obstacle.

"The Korean won is not deliverable offshore. Even more concerning, onshore liquidity during the extended FX trading hours remains largely insufficient to support tight execution at standards comparable to those observed in developed markets."

The message was straightforward: global investors still do not believe they can trade the won with the same depth, consistency and predictability available in developed-market currencies.

That distinction matters because hopes have grown in Seoul that MSCI inclusion could strengthen both equities and the currency.

The won has remained under pressure despite the stock rally, closing at 1,544.70 per dollar on Tuesday, down 2.4 percent from the end of May and more than 7 percent weaker than at the beginning of the year.

President Lee Jae Myung frowned at what he called the won's "excessive" weakness relative to Korea's economic fundamentals, while Finance Minister Koo Yun-cheol attributed the move to foreign investors' profit-taking and portfolio rebalancing.

Government officials maintained a brave face Wednesday, saying MSCI recognizes Korea's reform efforts and that continued progress should eventually lead to an upgrade.

Foreign investors must convert money into won to buy Korean stocks and convert it back when they sell. Yet the currency remains unavailable in a fully deliverable offshore market, while liquidity during extended trading hours has yet to prove itself.

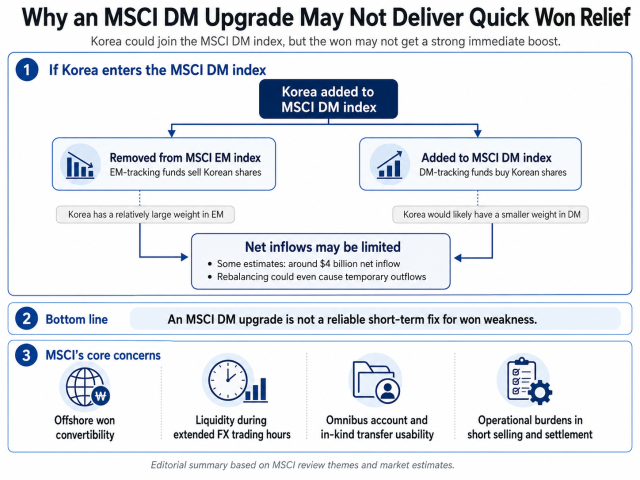

MSCI also cited the limited use of omnibus accounts and in-kind transfers, as well as operational burdens surrounding short selling and settlement procedures.

The issue, in other words, is not whether foreign money can enter Korea. It is whether investors can trade Korean assets, hedge currency risk and move capital without unusual friction.

That is also why MSCI inclusion should not be viewed as a straightforward remedy for won weakness.

If Korea joins the developed-market index, it would simultaneously leave the emerging-market benchmark. Funds tracking emerging-market indexes would have to sell Korean stocks, while developed-market funds would buy them.

The net effect may be far smaller than many assume.

Korea carries a relatively large weighting in emerging markets. In developed-market benchmarks, however, it would become a much smaller component alongside the United States, Japan and major European economies.

Some estimates suggest net inflows could amount to around $4 billion after offsetting the two streams, while others point to temporary net outflows depending on the timing and mechanics of rebalancing.

That makes MSCI inclusion a poor candidate for a short-term defense against currency weakness.

The Bank of Korea echoed that view Wednesday.

An upgrade could still produce meaningful long-term benefits. It would help reduce the Korea discount and strengthen the country's standing among global investors.

But that would be the result of a more open and predictable market structure, not a policy tool capable of stabilizing the exchange rate on its own.

The debate over whether the won must become something close to a reserve currency also risks missing the point.

A Bank of Korea official, speaking on condition of anonymity, said MSCI is not asking Korea to turn the won into another dollar, euro or yen.

"The issue is whether global institutional investors can convert, hedge and settle the won without being constrained by time zones or trading restrictions," the official said.

That may be the clearest takeaway from this week's decision.

MSCI is not questioning Korea's economic strength. It is questioning whether Korea's currency and market infrastructure are open enough for global investors to operate seamlessly.

Korea may eventually secure a developed-market upgrade if reforms continue. But this week's setback shows that such a milestone would be the outcome of structural reforms, not a shortcut to a stronger won.

Copyright ⓒ Aju Press All rights reserved.