Compared with the wild swings in equities and the won's slide to near three-decade lows, South Korea's bond market has remained remarkably stable, supported by steady foreign inflows since the country's sovereign debt joined the FTSE Russell World Government Bond Index in April.

The bond rally has also brought the Bank of Korea's terminal rate back into focus, with investors increasingly questioning how far the central bank can tighten policy when sluggish domestic demand remains masked by the semiconductor-led export boom.

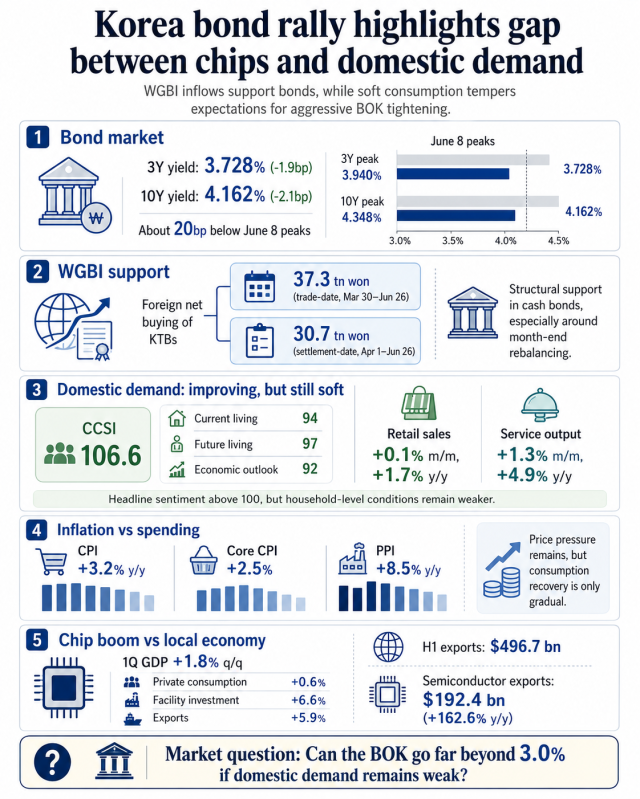

The three-year government bond yield fell 1.9 basis points to 3.728 percent by midday Friday, while the benchmark 10-year yield dropped 2.1 basis points to 4.162 percent.

Both yields are now about 20 basis points below their June 8 peaks of 3.940 percent for the three-year yield and 4.348 percent for the 10-year benchmark.

Unlike the equity market, battered by record foreign selling, the bond market has attracted steady foreign inflows.

According to the Ministry of Economy and Finance, foreign investors bought a net 37.3 trillion won ($26.9 billion) of Korean government bonds on a trade-date basis between March 30 and June 26 following WGBI inclusion. On a settlement-date basis, net purchases totaled 30.7 trillion won between April 1 and June 26.

The WGBI effect has been most visible in the cash bond market and around month-end portfolio rebalancing rather than in every intraday move.

On June 30, traders cited foreign futures buying, month-end WGBI demand and solid absorption of a 30-year government bond auction as drivers of a broad rally.

Foreign investors on Friday bought three-year government bond futures but sold 10-year contracts, suggesting the day's rally was driven not only by WGBI-related inflows but also by improving domestic and global market conditions.

The recent strength in bonds therefore reflects a combination of structural foreign demand and growing confidence that the Bank of Korea may not need to tighten policy much beyond 3 percent.

Inflation, the weak won, rising home prices and household debt all provide arguments for further tightening.

At the same time, softer consumption, fragile small businesses and uneven domestic demand continue to raise doubts about how restrictive monetary policy can become without weighing excessively on the broader economy.

The more important question is whether policymakers can justify pushing rates above that level and maintaining restrictive policy for an extended period.

The central bank has left that option open.

At its May policy meeting, the Bank of Korea kept its benchmark rate unchanged at 2.50 percent. Two Monetary Policy Board members dissented in favor of a 25-basis-point increase, while the central bank raised its 2026 growth forecast to 2.6 percent and its inflation forecast to 2.7 percent.

The next policy meeting is scheduled for July 16.

Governor Shin Hyun-song said in mid-June that inflation was likely to remain above target for a considerable period and that policy should respond in a timely manner to preserve price stability.

Economists remain divided over how high rates may eventually rise.

ING economist Kang Min-joo said the Bank of Korea had moved closer to another increase but cautioned that the benefits of the semiconductor-led expansion might not spread evenly across the broader economy. Higher energy costs and inflation could weigh disproportionately on services and construction, supporting a more gradual tightening path.

Some domestic analysts still expect the policy rate to reach 3.25 percent. Cho Yong-gu of Shinyoung Securities and Kong Dong-rak of Daishin Securities said the Bank of Korea's updated policy guidance and increasingly hawkish communication strengthened the case for two additional hikes this year, bringing the benchmark rate to 3.00 percent by year-end and 3.25 percent in early 2027.

Kim Myung-sil of iM Securities and Yoon Yeo-sam of Meritz Securities pointed to the Bank of Korea's August forecast revision as the next key milestone. Another upward revision to growth and inflation projections could shift the median policy outlook toward 3.25 percent or encourage more board members to support rates above that level.

Woori Financial Research Institute has taken an even more aggressive view, projecting two rate hikes in the second half of this year and two more in the first half of next year, lifting the benchmark rate to 3.50 percent.

The divergence in forecasts reflects an increasingly uneven recovery.

The Bank of Korea's composite consumer sentiment index rose 0.5 point to 106.6 in June, remaining above the long-term average of 100. Beneath the headline improvement, however, the picture was less encouraging.

Current living conditions stood at 94, expectations for future living conditions at 97 and the outlook for the broader economy at 92, all below the neutral threshold. While booming equity markets and exports have lifted overall sentiment, households remain considerably less optimistic about their own finances and the domestic economy.

Producer prices have also stayed elevated. The producer price index rose 0.8 percent from the previous month and 8.5 percent from a year earlier in May, reflecting broad-based increases in both industrial goods and services and adding further cost pressures on businesses.

Retail spending has improved only marginally. Retail sales edged up 0.1 percent from April and 1.7 percent from a year earlier in May. Sales of durable goods, including automobiles, declined both on a monthly and annual basis, offset by gains in semi-durable and non-durable goods.

Service-sector output rose 1.3 percent from the previous month and 4.9 percent from a year earlier in May, driven largely by financial and insurance activities as the stock market rally boosted trading and related services.

The economy expanded a stronger-than-expected 1.8 percent in the first quarter from the previous three months, led overwhelmingly by semiconductors and related investment. Private consumption rose just 0.6 percent, compared with a 6.6 percent increase in facility investment and a 5.9 percent rise in exports driven largely by information technology products and semiconductors.

Exports reached a record $496.7 billion in the first half, with semiconductors accounting for nearly half of total shipments, raising hopes that annual exports could surpass the $1 trillion milestone for the first time.

In contrast, nearly 976,000 businesses closed last year, with an overall closure rate of 8.64 percent. Among six major small-business sectors, the closure rate reached 11.08 percent, led by retail at 15.40 percent and restaurants at 15.14 percent. More than half of all closures were attributed to deteriorating business conditions.

In May, the number of self-employed people with employees rose by 80,000 from a year earlier, while those without employees increased by 29,000, pointing to continued business turnover but persistently weak profitability.

For now, the bond market is looking beyond the chip boom, betting that weak domestic demand will keep inflation contained enough to make an aggressively restrictive monetary policy unnecessary.

Copyright ⓒ Aju Press All rights reserved.