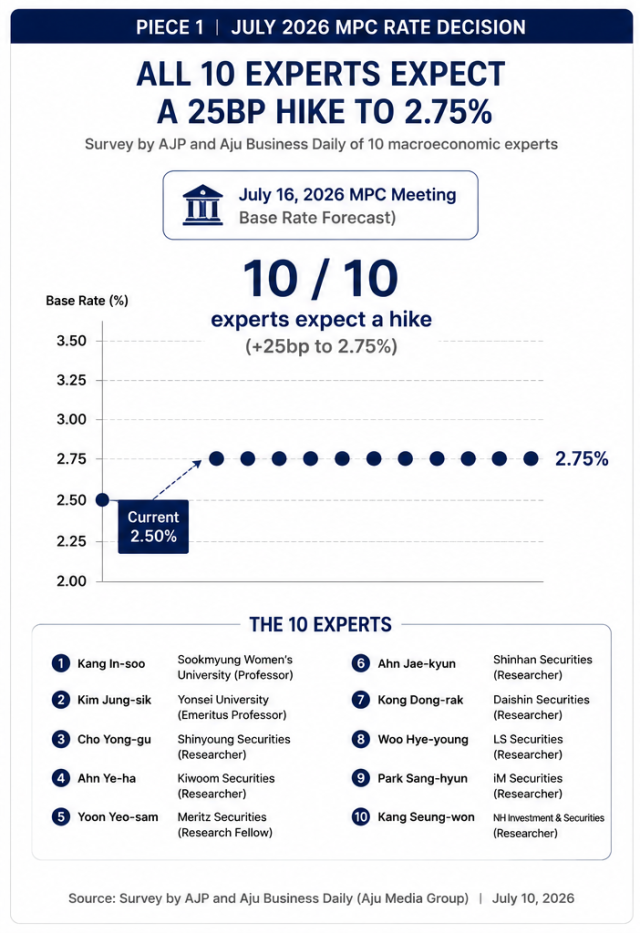

All 10 economists surveyed by AJP forecast the Monetary Policy Board will raise the benchmark interest rate by 25 basis points to 2.75 percent from 2.50 percent at its July 16 meeting, marking the central bank's first rate increase since January 2023.

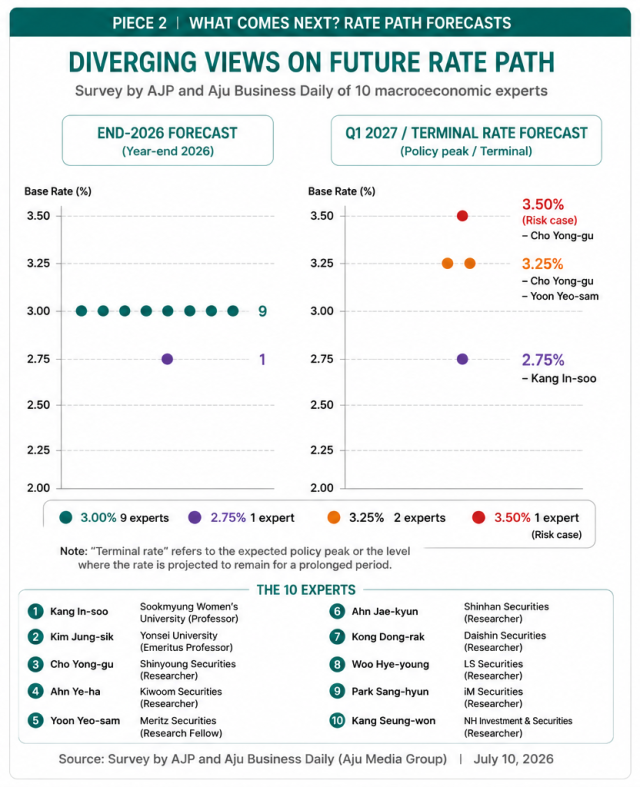

Consensus begins to fade only after next week's meeting.

Nine respondents expect the policy rate to reach 3.00 percent by the end of 2026, while two also see another increase to 3.25 percent in the first quarter of next year. Kang In-soo, professor of economics at Sookmyung Women's University, is the lone respondent expecting the rate to remain at 2.75 percent through year-end.

Persistent inflation above the Bank of Korea's target, a stronger growth outlook driven by the semiconductor boom, continued weakness in the won, accelerating house prices in the Seoul metropolitan area and faster household-credit growth were repeatedly cited as justification for resuming monetary tightening.

Several economists also said the central bank had already prepared markets for a rate increase through recent policy communications, including its May meeting, inflation assessment and anniversary remarks.

Cho Yong-gu of Shinyoung Securities expects inflation to remain above 3 percent through August despite falling oil prices, arguing that easing supply-side pressures alone would not remove concerns over underlying demand-driven inflation.

He also expects the Bank of Korea to pause in August before delivering another 25-basis-point increase in October, bringing the benchmark rate to 3.00 percent.

Yoon Yeo-sam of Meritz Securities also expects the benchmark rate to reach 3.00 percent by December before rising to 3.25 percent during the first quarter of 2027. He believes further tightening would help contain inflation while supporting exchange-rate and broader financial stability, although he sees limited justification for rates rising as high as 3.50 percent given weak employment and pressure on small businesses and the self-employed.

Kim Jung-sik, professor emeritus at Yonsei University, likewise expects two increases this year, citing stronger inflation, improved economic growth, buoyant asset markets and the need to limit capital outflows and further depreciation of the won.

Kang remains the most cautious respondent.

While agreeing that renewed housing-price gains and household borrowing warrant a July increase, he expects the move to mark the end of the tightening cycle this year, arguing that weak domestic demand outside the semiconductor sector and continued pressure on retailers, restaurants and other service businesses leave little room for substantially higher borrowing costs.

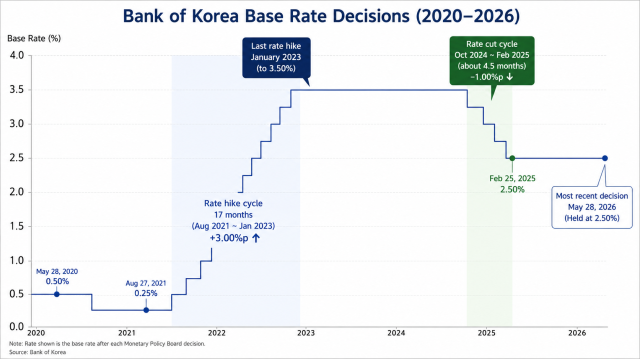

After holding the rate at 3.50 percent for about 21 months, the central bank began easing in October 2024 and lowered the rate by a cumulative 1.00 percentage point to 2.50 percent by May 2025 over roughly eight months. It has since kept the rate unchanged at 2.50 percent, including at its latest meeting on May 28.

The divergence widens beyond 3.00 percent.

Cho and Yoon both see 3.25 percent as the most likely terminal rate during the first quarter of next year, although Cho also sees a scenario in which rates eventually rise to 3.50 percent should growth accelerate further or financial-stability risks intensify.

The survey therefore points to broad agreement on the July decision but much greater uncertainty over how far the tightening cycle ultimately extends.

Whether the Bank of Korea continues raising rates beyond this year is likely to depend on whether Korea's semiconductor-led expansion can continue to offset weak domestic demand while preventing inflation, household debt and currency pressures from becoming more entrenched.

Copyright ⓒ Aju Press All rights reserved.