One channel of household leverage is being restricted just as another could be opened.

Household lending at the country's five largest banks - KB Kookmin, Shinhan, Hana, Woori and NH NongHyup - excluding government-backed loans rose by 3.697 trillion won (US$2.46 billion) to 647.578 trillion won at the end of June from 643.882 trillion won at the end of last year, according to banking industry data.

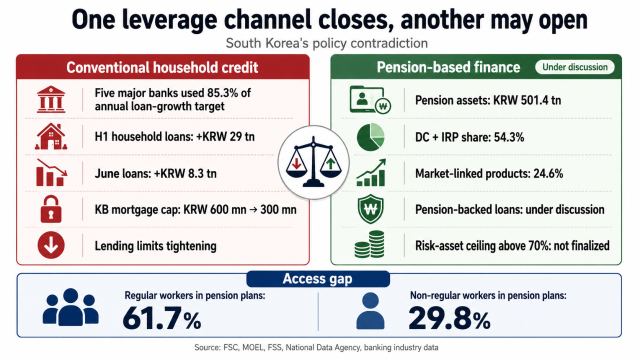

The increase represented 85.3 percent of the lenders' combined annual household loan growth target of 4.336 trillion won, leaving them with limited room to expand credit in the second half.

The targets are not statutory lending caps but management plans submitted by financial institutions in line with the government's household debt policy.

Household lending across the financial sector increased by 29 trillion won in the first half, including 8.3 trillion won in June alone, according to the Financial Services Commission.

Mortgage lending rose by 4.5 trillion won in June, while other borrowing, including unsecured credit, increased by 3.7 trillion won.

The FSC has instructed financial institutions to review their second-half lending strategies and monthly and quarterly management plans, warning that home transactions and previously approved group loans could keep mortgage growth elevated.

Banks have already begun raising borrowing barriers, with KB Kookmin Bank cutting the maximum amount available for home-purchase mortgages to 300 million won from 600 million won and some lenders restricting unsecured loans or reducing overdraft limits.

The pullback is likely to weigh most heavily on households that need new credit, rather than existing assets, to enter the property or financial markets.

The Ministry of Employment and Labor has said, however, that neither pension-backed lending nor a phased increase in the risk-asset ceiling has been finalized.

Current law generally prohibits the transfer, seizure or pledging of retirement pension benefits, while allowing them to be used as collateral in limited cases prescribed by presidential decree, including home purchases.

Financial institutions have rarely offered such products because of strong legal protections for pension benefits and uncertainty over how collateral rights could be enforced in the event of default.

Supporters argue that people facing urgent cash needs should be able to borrow against their retirement savings rather than permanently withdraw money from their accounts.

The number of people making early withdrawals from retirement pension accounts rose 4.3 percent to 67,000 in 2024, while the amount withdrawn increased 12.1 percent to 2.7 trillion won, according to the National Data Agency.

Home purchases accounted for 56.5 percent of withdrawals by number and rental housing deposits another 25.5 percent, putting the share of housing-related withdrawals above 80 percent.

Replacing early withdrawals with secured loans could allow account holders to meet temporary funding needs while keeping their retirement assets invested.

Outstanding retirement pension assets surpassed 500 trillion won for the first time at the end of last year, rising 16.8 percent to 501.4 trillion won, according to the Labor Ministry and the Financial Supervisory Service.

Defined contribution plans and individual retirement pension accounts, in which participants make their own investment decisions, accounted for 54.3 percent of the total, while market-linked products represented 24.6 percent.

If the proposed changes are introduced, people with sufficient pension balances could raise cash without withdrawing their savings or increase their exposure to equities and other risk assets.

The opportunity, however, would not be equally available to all workers.

As of June 2025, 61.7 percent of regular workers were enrolled in retirement pension plans, more than double the 29.8 percent rate among non-regular workers.

People with stable employment and long contribution records would be better placed to use pension assets as collateral or investment capital, while workers outside the system or with small balances would have little to leverage.

A retirement pension industry official who requested anonymity said the two policies should be viewed separately because "pension-backed loans are intended to preserve retirement assets by reducing early withdrawals," while conventional household lending controls are designed to curb excessive flows into property and equity markets and contain financial stability risks.

Replacing withdrawals with loans would not eliminate households’ funding shortages or debt-servicing burdens, while borrowers who fail to repay could ultimately damage their future retirement income.

If pension-backed loans are used to finance property or financial asset purchases, leverage that the government is attempting to suppress through conventional lending channels could simply re-emerge through retirement accounts.

The policy could therefore send a mixed signal by restricting borrowing against income and future earnings while making it easier to borrow against accumulated pension wealth.

It could also reinforce disparities between people who need credit to acquire their first meaningful assets and those who already hold assets that can be pledged or invested.

Regulators would need to determine whether pension-backed loans should count toward financial institutions’ household loan growth targets and borrowers' debt service ratios.

Clear rules would also be required on eligible borrowing purposes, collateral limits and the protection of pension benefits in the event of default, while any increase in the risk-asset ceiling would need to account for differences in pension balances and investment capacity.

Without such safeguards, the government could end up curbing one form of household leverage while encouraging another, shifting debt rather than reducing it and allowing existing wealth to determine access to the next round of financial opportunity.

Copyright ⓒ Aju Press All rights reserved.