Now the colony is on the move.

The tech-heavy junior market, which recently turned 30, has retreated more than 10 percent so far this year, ranking among the world's weakest performers, while the benchmark KOSPI has surged more than 82 percent.

Its sluggish performance owes much to the desertion of its primary players — the ants who have jumped ship to ride the AI wave sweeping the bigger bourse.

Individual investors who once chased aggressive returns in biotech, healthcare and other growth stocks on the KOSDAQ are increasingly migrating to large-cap semiconductor bets on the main bourse, drawn by the artificial intelligence boom and newly launched single-stock leveraged exchange-traded funds tied to Samsung Electronics and SK hynix.

Since leveraged ETFs linked to the two chip giants debuted on May 27, the KOSDAQ has set seven new yearly lows. Over the same period, the KOSPI gained 2.3 percent, while the junior market fell 8.8 percent.

According to Koscom's ETF CHECK, KODEX KOSDAQ150, the country's largest ETF tracking the KOSDAQ150 index, was down 13.9 percent over the past month as of Wednesday afternoon, underscoring broad weakness across the junior market.

The contrast is also visible in long-short strategies.

KODEX 200 Long KOSDAQ150 Short Futures, which benefits when large-cap shares outperform the junior market, returned 9.04 percent over the past month. Its mirror strategy, KODEX KOSDAQ150 Long KOSPI200 Short Futures, lost 12.63 percent.

The shift extends beyond market performance.

Investor deposits — cash held in brokerage accounts for future stock purchases — fell to 112.2 trillion won as of Monday, down from 139.7 trillion won a month earlier and the lowest level in nearly three months. Over the past month, retail investors also turned net sellers of KOSDAQ shares, unloading a net 1.41 trillion won.

Trading activity tells the same story.

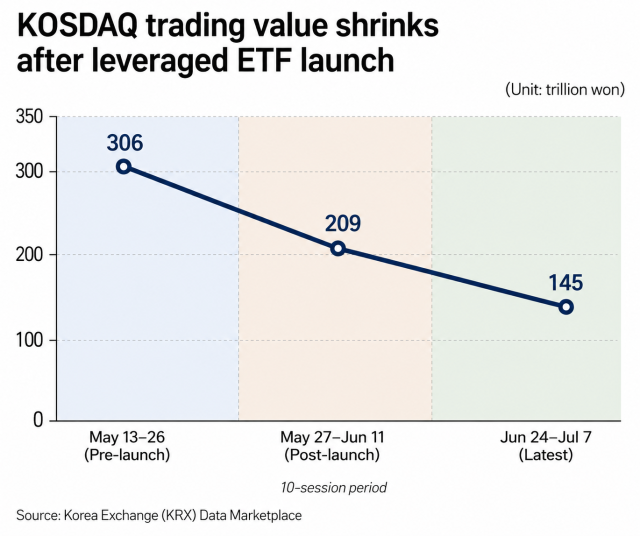

According to Korea Exchange Data Marketplace, total KOSDAQ trading value fell from about 306 trillion won during the 10 trading sessions from May 13 to May 26, immediately before the ETF launch, to 209 trillion won during the following 10 sessions from May 27 to June 11. It declined further to 145 trillion won during the latest 10-session period from June 24 to July 7.

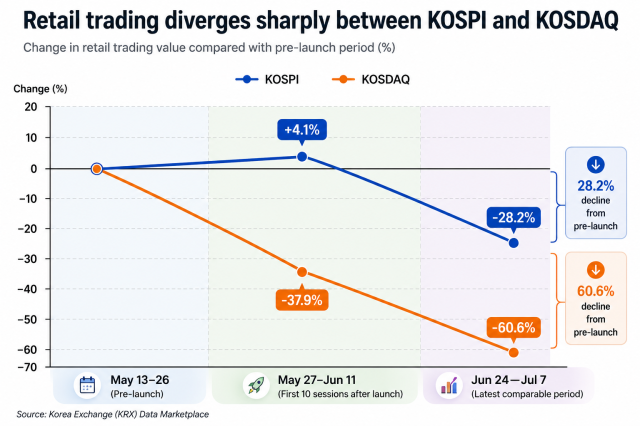

Retail trading showed an even sharper contrast.

During the first 10 trading sessions after the May 27 launch, retail trading value on the KOSPI rose 4.1 percent from the preceding 10-session period, while retail trading on the KOSDAQ fell 37.9 percent. By the latest comparable period, retail trading on the junior market had dropped 60.6 percent from its pre-launch level, compared with a 28.2 percent decline on the KOSPI.

Retail investors account for roughly 79 percent of KOSDAQ trading volume, according to KRX data, making changes in their behavior a key measure of liquidity and sentiment. During the retail-investing boom sparked by the COVID-19 pandemic in 2020 and 2021, individual investors accounted for 84 percent to 87 percent of KOSDAQ trading.

Traditionally, investors seeking high-risk, high-return opportunities gravitated toward biotechnology, healthcare and other growth companies listed on the KOSDAQ. Leveraged exposure to Korea's two largest semiconductor companies has now provided an alternative: speculative upside backed by strong earnings and the global AI investment boom.

Whether the shift proves temporary or structural remains unclear. But as long as retail money remains concentrated in chip-linked products and fresh cash stays thin, a meaningful KOSDAQ recovery may remain elusive.

The KOSDAQ closed Wednesday 5.56 percent down at 785, far below its debut at 1,000 points on July 1, 1996.

Copyright ⓒ Aju Press All rights reserved.