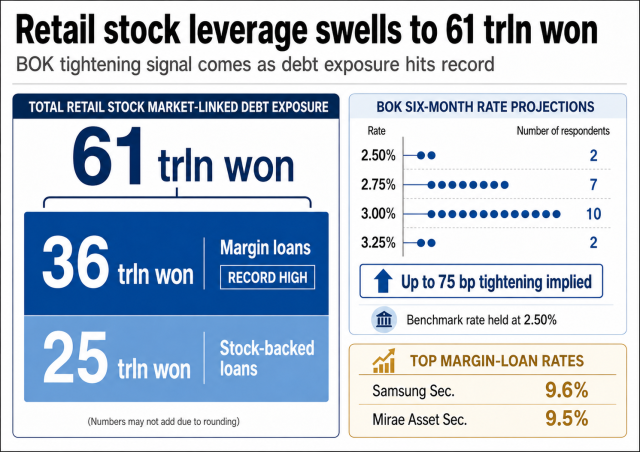

SEOUL, May 29 (AJP) — More than 60 trillion won ($39.9 billion) of leverage tied to South Korea’s stock market frenzy is emerging as a risk factor for both equities and the foreign-exchange market after the central bank all but signaled at least one rate hike in the second half.

“While demand curves typically slope downward, heavy debt-fueled investment could reverse that pattern, as forced liquidations are triggered and funds are withdrawn when prices decline,” Bank of Korea Governor Shin Hyun-song said Thursday after the central bank left its benchmark rate unchanged at 2.50 percent for a full year.

For ordinary investors, the message was straightforward: excessive leverage can accelerate capital flight and magnify market losses when sentiment turns.

The vicious cycle created by debt-financed investing can also hurt investors who have committed only their own funds. Shin’s remarks suggested that leveraged trading is no longer merely a retail-investor issue but a potential complication for monetary policy and financial stability.

The Bank of Korea’s latest dot plot, which contains three six-month rate projections from each board member, showed 10 dots at 3.00 percent, seven at 2.75 percent and two at 3.25 percent. Only two projected the benchmark rate remaining at 2.50 percent.

The distribution leaves room for as much as 75 basis points of additional tightening in the second half, a prospect that coincides with record borrowing in the domestic stock market.

As of Wednesday, outstanding margin loans had surpassed 36 trillion won, setting a new record. Stock-backed loans, in which investors borrow against existing holdings, also exceeded 25 trillion won, bringing retail investors’ total stock market-linked debt exposure to roughly 61 trillion won.

At the same time, borrowing costs have climbed sharply. Maximum margin-loan rates at major brokerages are already in the mid-to-high 9 percent range, with Samsung Securities charging as much as 9.6 percent and Mirae Asset Securities up to 9.5 percent.

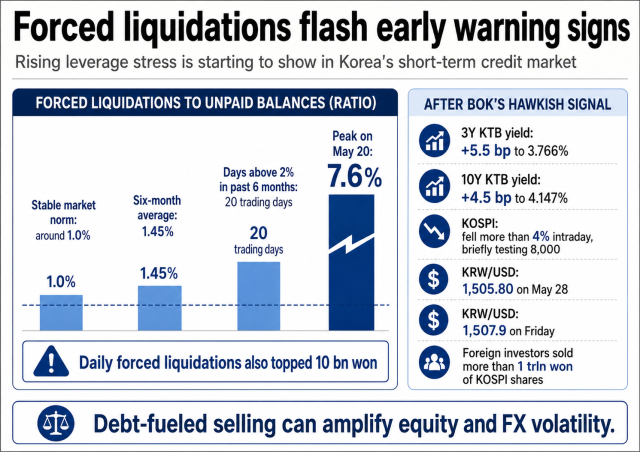

Those elevated rates could weigh on investor sentiment and erode borrowers’ ability to service interest payments even before stock prices begin falling. Early warning signs are already appearing in the short-term credit market, where forced liquidations have been rising in the three-day settlement segment.

Over the past six months, the ratio of forced liquidations to unpaid balances exceeded 2 percent on 20 trading days. The figure typically hovers around 1 percent in stable market conditions, but its six-month average has risen to 1.45 percent and spiked to 7.6 percent on May 20.

Market participants worry that stress in the short-term credit segment could spill over into the broader margin-loan and stock-backed lending market. If share prices fall, collateral values would decline, potentially triggering margin calls and forced selling by investors unable to meet collateral requirements.

Analysts also warn that debt-fueled positions could amplify volatility.

“Margin trading volumes are expanding too rapidly at a time when stock market volatility is also rising, pushing daily forced liquidations above 10 billion won,” said Lee Hyo-seop, a senior research fellow at the Korea Capital Market Institute.

“We need to monitor whether forced liquidations at one brokerage could spread to other firms and further increase volatility,” Lee said, warning that retail losses could evolve into broader market selling pressure.

The risk is heightened by the narrow nature of the KOSPI rally. Much of the index’s recent advance has been concentrated in a handful of semiconductor heavyweights, including Samsung Electronics and SK hynix, creating what some analysts describe as an index illusion that leaves leveraged investors more vulnerable if leadership stocks retreat.

The BOK’s tightening signal also carries implications for the foreign-exchange market. In theory, higher domestic rates should support the won by narrowing interest-rate differentials with major economies.

Shin separately addressed currency markets, warning against one-sided moves in the won.

“We will respond firmly to excessive one-sided movements in the exchange rate,” he said. “We will not tolerate herd behavior in the currency market. We have the tools, the will and various ways to respond.”

Yet if monetary tightening coincides with a sharp equity correction, the currency effect could become more complicated. Even as domestic rates rise, foreign investors may cut risk exposure, sell Korean stocks and increase demand for dollars.

That dynamic was visible following the BOK’s hawkish signal on May 28. In the bond market, the three-year government bond yield rose 5.5 basis points to 3.766 percent, while the 10-year yield climbed 4.5 basis points to 4.147 percent.

Stocks also came under pressure. The KOSPI tumbled more than 4 percent intraday, briefly testing the 8,000 threshold, while the won weakened to close at 1,505.80 per dollar.

Despite the governor’s hawkish rhetoric, markets continued to move in the opposite direction on Friday. The won lost another 5.1 won to close at 1,507.9 per dollar as foreign investors dumped more than 1 trillion won worth of KOSPI shares amid a stronger U.S. Dollar Index fueled by expectations of a U.S.-Iran peace deal.

For that reason, investors increasingly view Shin’s message as more than a warning about retail leverage. It underscored how rising stock market debt has become a policy burden for the central bank, as tighter monetary policy, narrow market leadership and exchange-rate volatility can reinforce one another during a correction.

Shin signaled that the BOK would take those risks into account when determining the pace of tightening.

“The timing and pace of interest rate hikes will be decided based on incoming data, as we assess the expansion of inflationary pressures, the path of economic recovery and broader financial stability conditions,” he said.

Copyright ⓒ Aju Press All rights reserved.